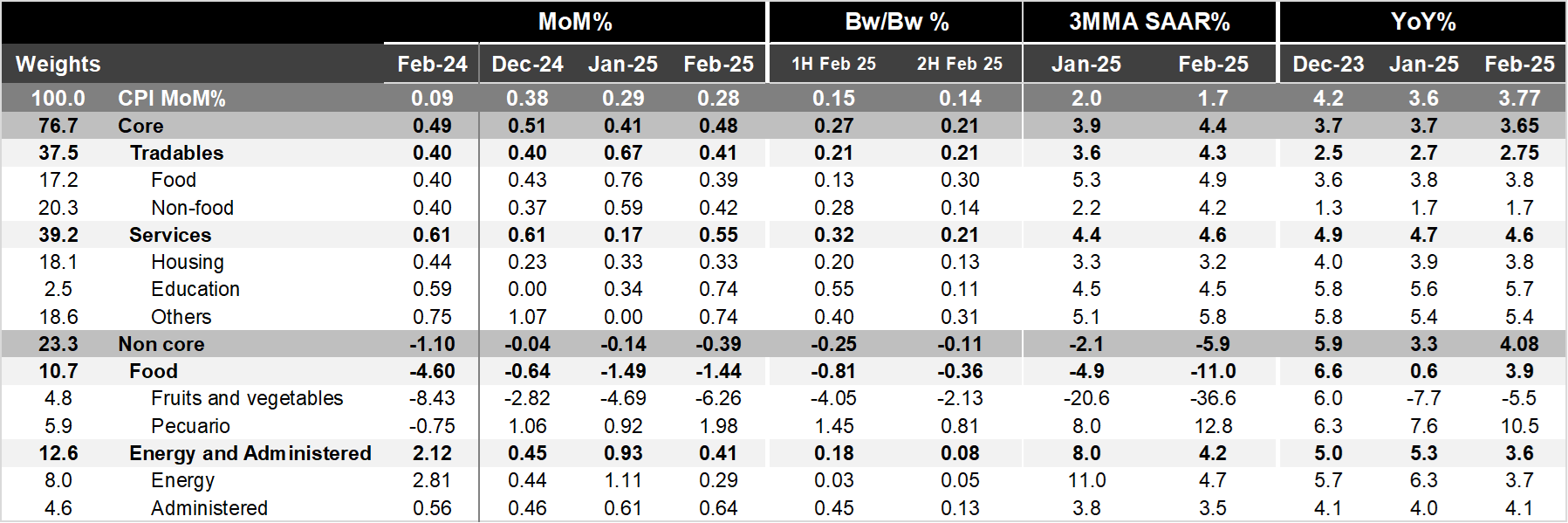

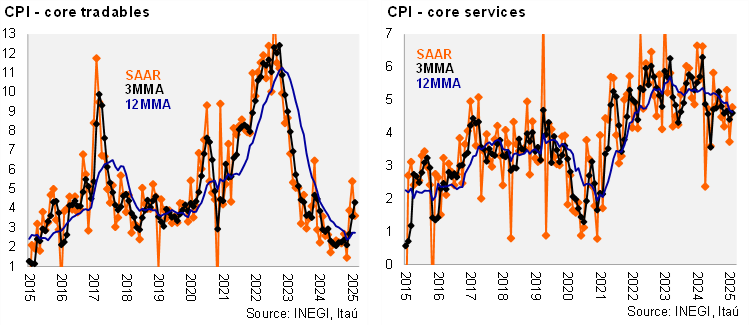

Bi-weekly headline CPI for the second half of February stood at 0.14%, higher than Bloomberg’s market consensus (0.10%) and lower than our forecast (0.23%). On the other hand, core inflation came at 0.21%, above consensus (0.16%) and our forecast (0.15%). Inside the core component, tradables prices stood at 0.21% 2w/2w, same as in the last fortnight. The main surprise came from services prices, which stood at 0.21% 2w/2w, from 0.32%, with some relief in education and housing, although still somewhat high in other services. The non-core component decreased by 0.11% 2w/2w mainly due to a deflation in agricultural prices despite seasonal patterns and a bird flu outbreak in the US, with pressures relief in prices of tomato, onion, and potato, while energy and government tariffs increased a bit during the fortnight (0.08%).

In annual terms, headline inflation accelerated to 3.77%, from 3.59% in January, but still below the ceiling of Banxico’s target. Core CPI was a bit down, from 3.66% in the previous month to 3.65% now, with merchandise at 2.75% (from 2.74%) and services at 4.64% (from 4.69%). In the February 6th statement, Banxico forecasted 3.7% for headline and 3.6% for core during the 1Q25, close to January-February headline inflation at 3.6% and core at 3.4%.

Our take: Today’s print reinforces our view that the disinflationary trend is gaining momentum, supported by low agricultural prices and a slowdown in economic activity. However, the inflation outlook remains challenging, with the peso depreciation, volatile climate conditions with droughts in some parts of the country, and a tight labor market posing risks. We forecast CPI to end 2025 at 3.9%. For the interest rate, we maintain our call for a 50bps cut rate on March 27th, taking the interest rate to 9.0% and 25 bps after that, with the year-end forecast at 8.50%.