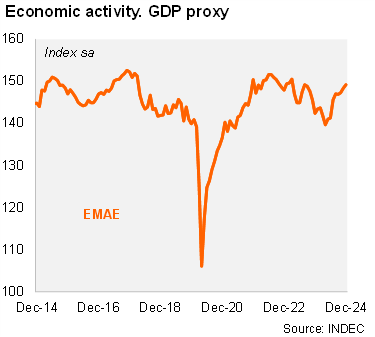

Activity rose sequentially in 4Q24, marking the second consecutive quarterly gain. According to the EMAE (official monthly GDP proxy), economic activity increased by 0.5% MoM/SA in December, following a 0.7% MoM/SA gain in November. Thus, activity increased by 1.2% QoQ/SA in December after growing by 4.1% QoQ/SA in September. On an annual basis, activity rose by 5.5% YoY in December and by 1.7% YoY in 4Q24 (vs. -2.1% YoY in 3Q24). We note that the seasonally adjusted GDP proxy exceeded the level of December 2023, leaving the recession behind, and showed a statistical carryover of 2.6% for 2025.

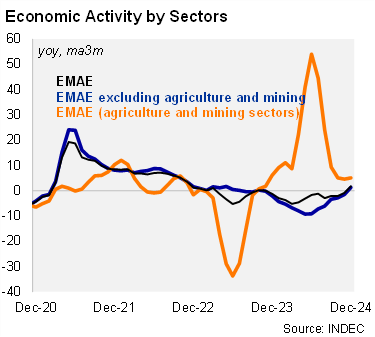

Mixed signals across sectors in 4Q24. On the positive side, primary activities increased by 5.1% YoY in 4Q24 (vs.+9.3% YoY in 3Q24), still reflecting the normalization of agriculture after a severe drought in 2023, while manufacturing grew by 0.5% YoY in the same period (vs. a drop of 5.9% YoY in 3Q24). On the other hand, construction activity fell by 12.4% YoY in the period (vs. -14.9% YoY in 3Q24), affected by the freeze on public-sector work, while services activity (including the commerce sector) fell by 1.2% YoY in the period (vs. -3.1% YoY in 3Q24).

Our take: We expect 4.5% growth in 2025. In our view, the recovery of real wages and lower interest rates are likely to support private consumption growth this year. On the demand side, the normalization of the international trade amid lower capital controls should be positive for several sectors. The national accounts data for 4Q24 will be published on March 19, while the January 2025 EMAE figures will be published on March 27.