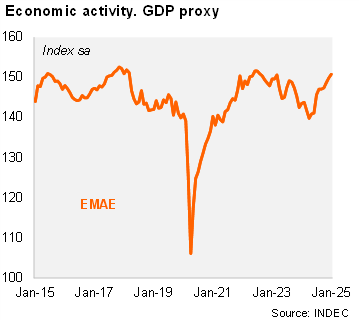

Activity rose sequentially in January, marking the fourth consecutive gain. According to the EMAE (official monthly GDP proxy), economic activity expanded by 0.6% MoM/SA, following a revised 0.80% MoM/SA growth in December (+0.5% in the previous report). Thus, activity expanded by 1.8% QoQ/SA in January, after growing 1.4% QoQ/SA in the previous month. On an annual basis, activity rose by 6.5% and by 4.3% in the quarter ended in January (+2.1% yoy in 4Q24). The annual figure was above the market forecast of 5.0%, as per the Bloomberg survey (median value).

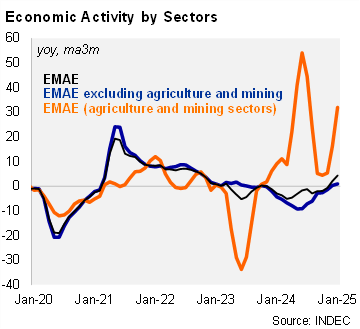

Most of the sectors rose on an annual basis. Primary activities rose by 32.0% YoY in the quarter ended in January (vs.+16.3% YoY in 4Q24), while manufacturing expanded by 3.4% YoY in the same period (vs. a gain of 0.7% YoY in 4Q24). Services (including the commerce sector) rose by 0.7% YoY in the period (vs. -0.4% in 4Q24), likely supported by the recovery of real wages. Construction fell by 7.0% YoY in the period (from -12.4% YoY in 4Q24), due to the strict control of public works.

Our take: We forecast 2025 GDP growth at 4.5%, with upside risks due to a high carryover and the expected improvement of demand-side components. On the demand side, the recovery in real wages and lower borrowing rates are likely to support private consumption. On the supply side, drought concerns have eased with the arrival of timely rains. The February 2025 EMAE figures will be published on 22 April.