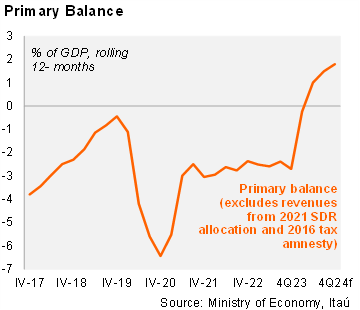

According to the Ministry of Finance, Argentina’s 2024 primary balance reached a surplus of 1.8% of GDP, while the nominal balance stood at +0.3% of GDP. In December, higher pension and wage bonuses expectedly led to a primary deficit of ARS 1.301 billion and a nominal deficit of ARS 1.557 billion, both well below December 2023. Based on these figures, we estimate a consolidated nominal deficit of around 1.7% of GDP in 2024 (including net interest payments from the central bank), narrowing significantly from a deficit of 14.0% in 2023.

Real tax revenues declined in 4Q24, but at a slower pace due to the recovery in economic activity at the margin. Tax collection increased by 3.9% yoy in real terms in the period, after dropping by 5.2% in 3Q24. Total real revenues decreased by 2.3% yoy in the period (-8.9% in 3Q24).

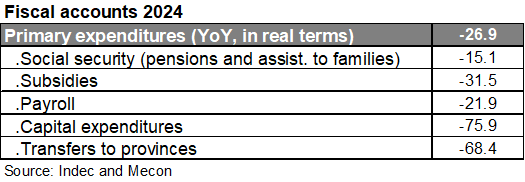

Strict control on expenditures continued in 4Q24. Primary expenditures declined by 22.1% yoy in real terms in the period, after falling 24.1% yoy in 3Q24. Energy subsidies fell by 29.6% yoy, compared with a drop of 12.8% in 3Q24, while payrolls decreased by 24.3% yoy (-20.8% in 3Q24). Capital expenditures were down sharply by 69.7% yoy (-74.7% in 3Q24) due to the freeze on public works, while transfers to provinces plunged by 63.3% yoy. Pension payments were up 3.2% yoy (-12.4% in 3Q24) due to a new adjustment formula based on inflation plus a one-time bonus.

Our Take: We expect a primary surplus of 1.3% of GDP in 2025, consistent with a balanced nominal budget, both in line with the 2025 budget bill. The government's strong commitment to the fiscal framework as the main anchor of the stabilization program supports our call. Fiscal data for January will be published on February 17, and we expect them to start the year with surpluses.