Never a dull moment. Argentina’s central bank surprised by announcing (see here) important changes to its exchange rate framework that have the objective of further reducing inflation, and boost investment, employment and activity over time. The main changes include:

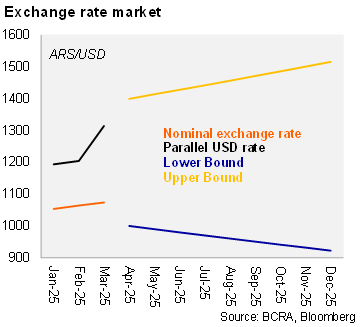

- The USDARS (trading at roughly ARS1078 last Friday), which was devaluing at a steady 1% monthly pace (since February), will be allowed to float within an exchange rate band between $1.000 and $1.400. The band’s limits will widen at a 1% MoM pace. When the exchange rate reaches the upper (lower) bound of the band, the BCRA will defend the band by selling (buying) dollars from (accumulating) reserves. Within the band, the BCRA may also intervene to mitigate volatility. Argentina had an exchange rate band during Macri’s administration;

- The dollar blend is eliminated, exchange rate restrictions on natural persons are also removed, and profits are allowed to be distributed to shareholders offshore starting with the financial year 2025, and payments on the foreign trade of goods is flexibilized;

- The nominal anchor is strengthened with no BCRA issuance to finance the fiscal deficit or for the remuneration of monetary liabilities.

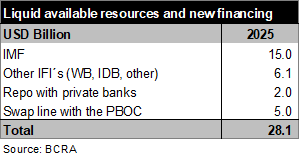

Big time support from the IMF... Following the IMF staff-level agreement earlier in the week for a USD20 billion program in the form of a 48-month Extended Fund Facility (EFF), the IMF’s Board of Executive Directors swiftly approved the program providing greater detail on the disbursement schedule (statement here). This is Argentina’s 23rd IMF agreement, and the third since 2018. Again, as per the official statement, “building on the authorities’ strong track record, the arrangement supports the transition to a new phase of their stabilization and growth plan to entrench macroeconomic stability, strengthen external sustainability, and deepen structural reforms to create a more open and market-oriented economy.” A total of USD12 billion will be immediately disbursed, with an additional USD2 billion following a June 2025 review. Argentina has expressed their intention of using these resources to pay down the MoF’s debt held by the central bank – strengthening its balance sheet – and maturities owed to the IMF from the previous program.

… and other international financial institutions (IFIs). The World Bank Group (statement here), in parallel, approved a USD12 billion package that also supports Milei’s economic reform program; this program combines sovereign support (USD5 billion), private sector development (up to USD5.5 billion), and guarantees to expand credit access (USD1.5 billion). The IDB issued a statement it would provide up to USD10 billion in support for Argentina over the next three years, of which USD7 billion would be for the public sector and USD3 billion to boost private sector activity. Last week, the BCRA also renewed the USD5 billion swap line with the PBOC.

The following table describes the BCRA’s estimate of liquid available resources and new financing:

Our take. Allowing for the currency to float within an exchange rate band takes place earlier than we anticipated, supported by an important backstop support from IFIs. The administration has made commendable efforts in the macro stabilization of the economy, delivering better and faster than expected results so far, and the next phase still has considerable challenges. We expected the “cepo” to be gradually removed by the end of the year, following the October mid-term elections; the earlier announcement might be linked to the sustained pressure the currency experienced in recent weeks in the FX spot market (net sales by USD2.4 billion since mid-March) that led net international reserves to close to -USD 9.5 billion). While the levels of the exchange rate band should allow for a correction of the real appreciation of the currency in recent quarters (as inflation exceeded the devaluation pace) and should facilitate investment inflows, the tradeoff is likely to be higher inflation, that, in turn, has been accelerating in recent months. The administration will likely down further on spending cuts, strengthen the fiscal anchor, and moderate the upside pressure on inflation expectations coming from projected exchange rate dynamics. In fact, the primary fiscal target for 2025 changed to a surplus of 1.6% of GDP, up from 1.3% before. The Secretary of the Treasury is scheduled to visit Argentina this week, and may announce further policy measures to support Milei’s reform program.