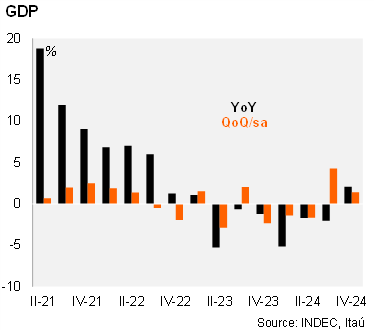

GDP expanded in 4Q24. Output increased by 1.4% qoq/sa, after growing by 4.3% qoq/sa in the previous quarter. Growth in the quarter was above the 1.2% outlined by the monthly GDP proxy (EMAE). On an annual basis, GDP grew by 2.1% in 4Q24, breaking a string of six consecutive quarterly contractions. Thus, in 2024, GDP fell by 1.7%, reflecting the effects of the stabilization program in the first half of the year, but with a strong recovery in the second half. Thus, the statistical carryover for 2025 stood at 2.7%.

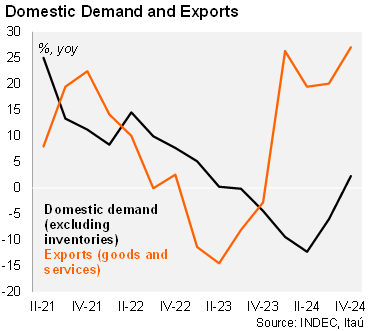

Final domestic demand – led by investment and private consumption – rose by 4.3% qoq/sa in 4Q24, from 5.0% in the previous quarter. Fixed investment increased by 11.3% in the quarter followed by an expansion in private consumption of 3.2%. Public consumption rose 0.8%. On an annual basis, domestic demand (excluding inventories) rose by 2.3% yoy, reflecting a 2.8% yoy increase in private consumption and a 1.9% gain in gross fixed investment. Moreover, public consumption expanded by 0.5%. Regarding external demand, exports increased by 27.1% yoy, while imports rose by 9.7% yoy.

Our take: We forecast 2025 GDP growth at 4.5%, with upside risks due to a high carryover and the expected improvement of demand-side components. On the demand side, the recovery in real wages and lower borrowing rates are likely to support private consumption. On the supply side, drought concerns have eased with the arrival of timely rains.