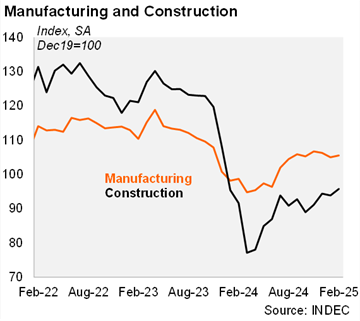

Manufacturing rose sequentially in February. The IPI manufacturing index increased by 0.5% mom/sa in February, after falling 1.2% mom/sa in January. However, industry output fell by 0.3% qoq/sa in the quarter ended in February, following a 1.9% expansion in 4Q24. On an annual basis, manufacturing rose by 5.6% in February, and by 7.3% in the quarter ended in that month. Seven of nine sectors grew in February on an annual basis, except for non-metallic and basic metallic minerals and petroleum refining, chemicals, rubber and plastics products. According to the INDEC survey, 31.7% of companies expect an annual increase in internal demand over the next three months, 30.4% expect a decline and 37.9% foresee no changes.

Construction also expanded in February. The construction index rose by 2.0% mom/sa in February, also after falling 0.6% mom/sa in the previous month. Moreover, construction rose by 4.1% qoq/sa in the quarter ended in February (-1.1% qoq/sa in 4Q24). Construction activity rose by 3.7% yoy in February and dropped 3.1% yoy in the quarter ended in that month. Employment in the sector contracted by 4.8% relative to January 2024 (figures have a one-month lag). According to a qualitative survey, 67.9% involved in private construction anticipate no changes in activity levels over the next three months. Meanwhile, 21.1% expect an increase, while 11.0% anticipate a decline. Among companies primarily engaged in public works, 16.5% anticipate a decrease in activity levels during the next three months, while 60.2% expect no change and 23.3% increase.

Our take: Even though global policy uncertainty remains elevated, and domestic financial conditions have experienced important swings as of late, the gradual recovery of economic activity, especially construction, continues. We forecast a snapback in 2025 GDP growth to 4.5%, mainly supported by high carryover, but also due to the improvement in real wages.