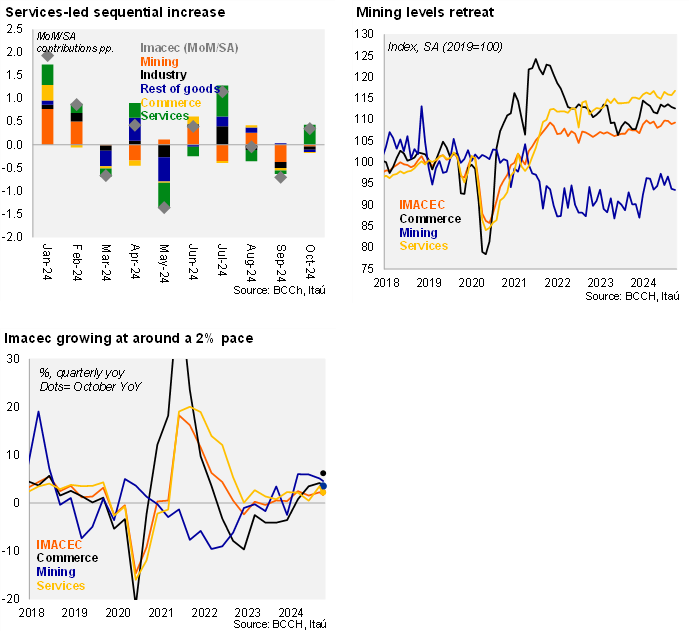

According to the Central Bank, the Monthly Index of Economic Activity (IMACEC) increased 0.4% MoM/SA, partially unwinding the two consecutive sequential declines in previous months. The annual variation came in at 2.3% (0.3% YoY in September). The activity performance was a notch below both the Bloomberg consensus and our 2.5%. The mining pull came in at 3.5%. Commerce grew 6.2%, lifted on the retail side by sales made through online platforms, particularly grocery stores and in specialized clothing stores. Meanwhile, wholesale commercial activity was boosted by machinery sales. Services were up 2.2%, supported by health and education. Overall, non-mining activity increased a 2.3% YoY (0.4% in September). If the economy maintains the October level towards the end of the year, GDP will expand by roughly 2.1% YoY (0.6% in 2023).

At the margin, the 0.4% activity uptick was explained by the 0.9% increase in business services (-0.2% in September). Commerce, mining and manufacturing all posted moderate declines from September. The economy rose 2.0% QoQ/SAAR, decelerating from the 2.8% in 3Q, while non-mining GDP increased 2.8% QoQ/SAAR (3.2% in 3Q).

The outlook remains challenging. Business sentiment deteriorated in November, commercial credit remains at low levels, while the market has incorporated a scenario of higher-than-expected interest rates and inflation globally. On the positive side, imports of capital goods have returned to growth, in line with the mild investment recovery anticipated. Outstanding real commercial loans in Chile contracted again in October by 4.7% YoY, after plummeting by 5.85% in September (-5.27% in October 2023), declining on an annual basis since May 2022. The fiscal scenario (accumulated nominal deficit of 2.5% of GDP as of October), will see a spending pullback at the backend of the year, while the approved 2025 budget saw a cut in real expenditure from the proposed to 2.7% to an approved 2%. Business confidence as measured by the IMCE edged down to 48.7 in October (50 = neutral), the lowest level this year. Meanwhile, non-mining sentiment remains at a lower 42.2 points. Imports of capital goods were up 3% and 10% YoY in September and October, while consumer goods imports are also up at a near double-digit rate.

Our Take: We expect the economy to grow 2.2% this year. A softer China growth outlook, and tighter than expected global financial conditions would keep growth downbeat next year (1.9%).