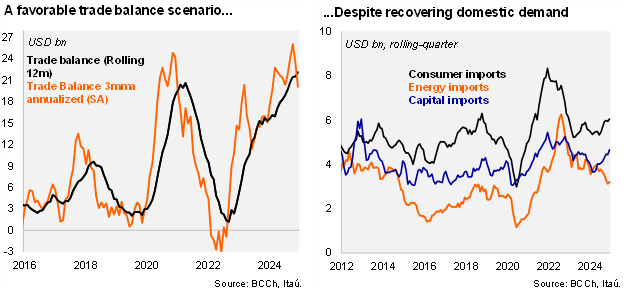

A USD 2.4 billion trade surplus was recorded in December, a USD 0.6 billion increase over one year. The surplus was broadly in line with our USD 2.5 billion call. The trade surplus in 2024 reached USD 22.1 billion (close to 7% of GDP; USD 15.3 billion in 2023), boosted by copper exports, while energy imports softened. The annualized quarterly trade balance sits just over USD 20 billion (SA). Annual trade surpluses of such magnitudes were last registered in 2006-2007.

Exports remained upbeat at the end of the year. Exports rose by 18.9% YoY (2.6% in November). Nominal copper exports rose 12.8% YoY (7.1% YoY in November; +17% in 2024). Lithium exports contracted 35.8% YoY (due to lower prices; -48% in 2024). Agricultural exports more than doubled, boosted by fruits (cherries to China). Manufacturing exports also ticked up by a robust 15.9% YoY (4.1% in November), lifted by foods, pulp and paper while chemical sales fell. During 2024, total exports increased 5.9%, unwinding the 4.1% drop in 2023. At the margin, exports during 4Q24 fell 4% (SA, annualized).

Signs of recovering domestic demand consolidated. Total imports rose by 14.6% YoY (2.5% in November). Energy-related imports were broadly flat from last year in December but dropped by around 10% during the full year, playing a key role in supporting the large trade surplus as the normalization of global energy costs advanced. Both imports of consumer goods (+15.6% YoY) and capital goods (+25.1% YoY; +5.8% in November) increased in December from last year, in line with a gradual recovery of private consumption and investment amid a scenario of lower average interest rates and inflation. Imports of machinery for mining and construction doubled over twelve months, in line with dynamics in recent months. For the full year, total imports fell 1-5% YoY (-16.4% in 2023), although consumer goods imports ticked up 3.4% (-23% in 2023), and the capital goods decline eased to -3.9% (-12.5% in 2023). At the margin, imports during 4Q24 accelerated to 14% (SA, annualized).

Our Take: The large trade surplus is supporting a narrow CAD (of around 2.5% of GDP in 2024). A gradual domestic demand recovery will support higher imports ahead, yet still favorable terms-of-trade favor upbeat expects and large trade surpluses, sustaining a narrow CAD into 2025 (2.6%).