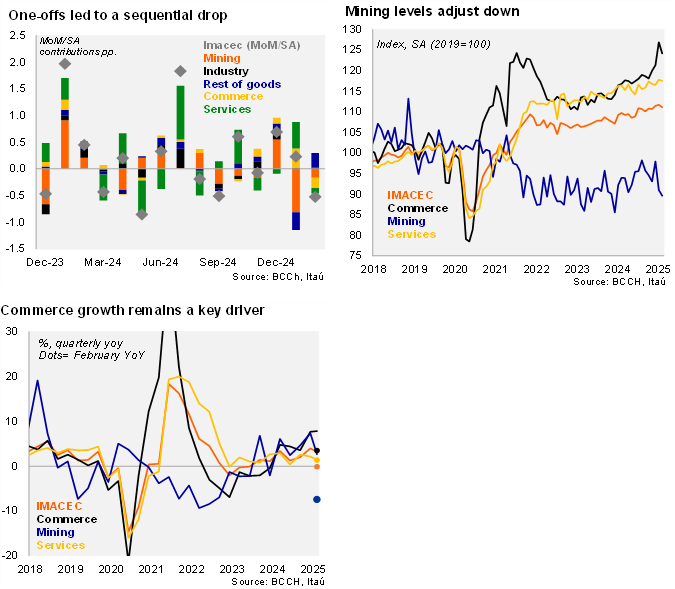

The monthly GDP proxy (IMACEC) was dragged down sequentially by mining, commerce, and services. Activity at the margin was hampered by the partial day nationwide blackout. Non-mining activity fell 0.4% MoM/SA, ending a four-month sequence of sequential gains. Activity was pulled down by the 2.2% MoM/SA commerce decline (0.2pp contribution). Mining fell 1.5% MoM/SA. Services ticked down 0.2% MoM/SA due to business services. On the goods production front, activity rose 0.4% MoM/SA. Overall, the economy contracted by 0.1% YoY in February, a tick below market expectations (Itaú: +0.2%; Bloomberg consensus: +0.1%; 2.3% in January). Non-mining activity increased by 0.9% YoY (2.8% in January). After adjusting for seasonal and calendar effects, the economy grew by 1.3% YoY, while non-mining activity rose by 2.1%

While the blackout hindered sequential dynamics, the 2024 leap-year resulted in a more challenging base effect for annual growth rates. Activity increased 3.1% YoY during the quarter ending in January, down from 4% in 4Q24. Mining production slowed to 2.6% YoY, well below the 7.3% in 4Q24. Commerce in the quarter continued to grow at an upbeat 7.8% YoY. Despite the 0.5% sequential drop in February, activity over the quarter rose by an elevated 3.3% QoQ/Saar (1.5% in 4Q). Non-mining activity increased at a higher 4.8% QoQ/Saar.

Our Take: After the December mining production surge (+5.3% MoM/SA), activity has softened, dropping 8.5% since the close of 2024. Mining was a key growth driver last year, rising 5.2%. We expect production to ease to 3-4%, but year-to-date dynamics have underwhelmed. Despite the February disruption that stalled several business operations, the upbeat tourism flows, and improved labor dynamics will likely support a commerce and services rebound in March. Growing global uncertainty has seen private sentiment shift down in March, with business confidence falling 5.5pp back into pessimistic territory. Nevertheless, data on the imports of capitals goods continue to signal a favorable investment performance ahead. Meanwhile, foreign tourism inflows to Chile rose by 55% YoY in February 2025 (67.3% in February) reaching roughly 649,000 tourists, the highest for the month of February since 2018. We expect IMACEC growth in March to be above 2%. The central bank will publish the March activity data on May 02. Our GDP growth estimate for 2025 is 2.3%, with an upside bias.