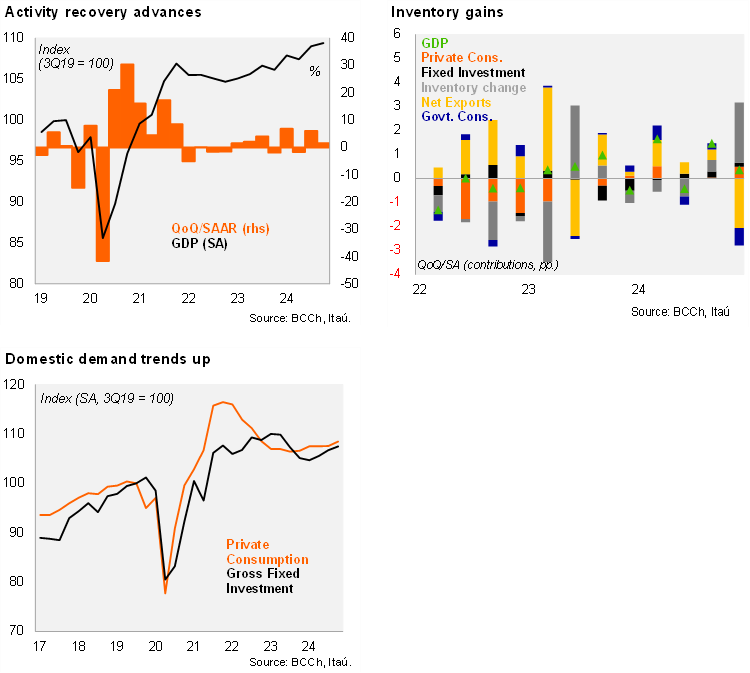

According to the BCCh's national accounts, Chile’s GDP rose by 4.0% YoY in 4Q24 (2% in 3Q24, -0.3pp revision), above the 3.7% performance outlined by the monthly GDP proxy (Imacec). Domestic demand increased by a larger 4.3%, pulled up by total investment (14.7% YoY), as the accumulation of inventories may signal the improvement in business sentiment. Gross fixed investment rose by 3.3% YoY, the first annual increase recorded since 2Q23. Both machinery and equipment (8.3% YoY) and construction (0.2%) registered annual gains. Private consumption rose 1.2% YoY (2.2% in 3Q), lifted by durable goods (9.8%) and services (1.4% YoY). Imports of goods and services increased at a double-digit rate, while export growth was lifted by agriculture (cherries). The mining export pull eased to 3% YoY, from 7.8% in 3Q. Sequentially, the economy increased 0.4% from 3Q24 (SA), adding to the 1.5% rise in 3Q. Growth in the quarter was pulled up by consumption (0.8% QOQ/SA), driven by durable goods and services, while construction lifted gross fixed investment (0.7% QoQ/SA). Public spending expectedly retreated in an effort to meet fiscal targets. Considering the new data, if GDP remains constant at 4Q24 levels throughout 2025, GDP growth this year would reach 0.9% (similar to the carryover at the start of 2024).

The economy grew by 2.6% in 2024, up from 0.5% in 2023. The 2024 rate was 0.1p higher than outlined by the Imacec. Meanwhile, the central bank revised GDP growth upwards by 0.1pp and 0.3pp for 2022 and 2023, respectively. As a whole, the economic recovery has been somewhat more robust than previously thought. During last year, net exports was a key growth contributor, adding 1.3pp to the overall increase. Total consumption added 1.1pp, with around half stemming from public spending. Gross fixed investment shave 0.4pp from activity. With domestic demand improving and global growth outlook more uncertain, the upside pull from net exports will likely moderate into 2025.

Our Take: Leading indicators of upbeat capital goods imports and improving business sentiment, along with elevated copper prices, improving credit dynamics and consumer tourism place an upside bias to our 2.3% 2025 GDP forecast. Improved activity dynamics will likely lead the BCCh to report a closed, or slightly positive, output gap (as opposed to somewhat negative in prior reports). Still high inflation, improved domestic demand and heightened global uncertainty will prevent the Board from cutting rates this year. Meanwhile, the persistence of the latest CLP rally has seen medium-term inflation expectations correct swiftly towards the target, easing prior market pressure to hike rates. We expect the BCCh to raise its 2025 GDP growth range from 1.5-2.5% to 2.0-3.0% when it publishes the March IPoM next week.