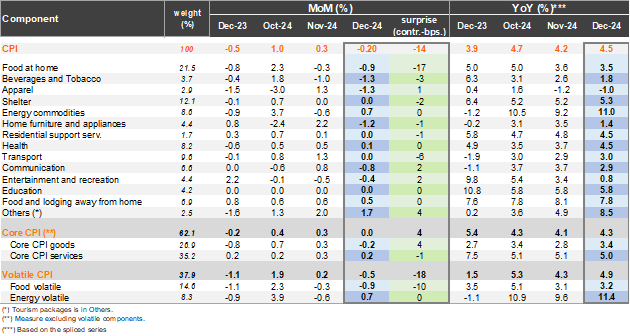

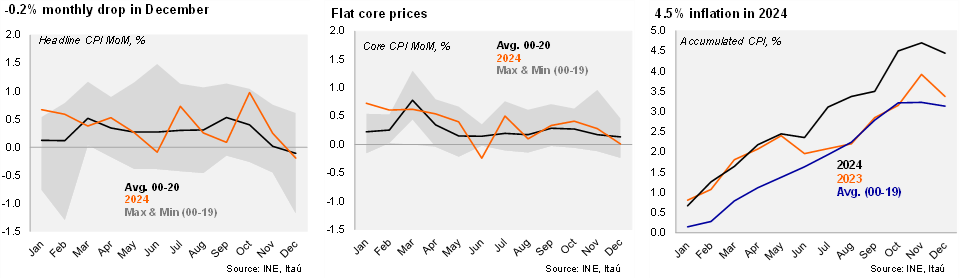

Consumer prices fell 0.2% from November, a larger decline than our -0.06% call, and the 0.0% Bloomberg consensus (implicit forecast in 4Q IPOM: +0.04%). The price drag in the month came mainly from volatiles that are likely to revert. The key declines came from the food and beverage division (-19bp contribution; led by potatoes , -17%), along with cyber sale led falls in the household goods and maintenance division (-5bps), information and communication (-5bps), apparel (-3bps) and alcohol beverages (-5bps). International air travel dropped 12% (-8bps). In contrast, local air travel prices rose 19% (+4bps), while liquid gas was a key upside driver (+5bps). Ex-volatile consumer prices were flat from November (implicit forecast in 4Q IPOM: +0.2%) as falling goods prices were offset by higher services. As in November, second-round effects of the rise in electricity prices and the increase in the minimum wage, among others, were not evident in the December data. Nevertheless, risks stem from the expected rise in electricity prices (near 10% in January), and the effects of the latest CLP strain (depreciation of around 7% in the last six months).

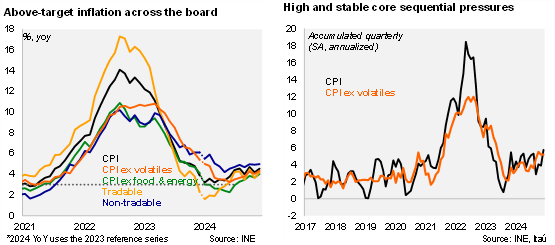

Core inflation pressures remain high. Inflation concluded 2024 at 4.5% (4.2% in November; below our 4.7% call; BCCH: 4.8%). Annual inflation has been above the 3% target since July 2024. Core inflation ended the year at 4.3% (4.0% in November; BCCh: 4.5%). Core goods dropped 0.2% (3% YoY), while core services rose 0.2% from November (5% YoY). Volatiles dropped 0.5% MoM, dragged down by declines in food prices, and leading to an annual increase of 4.9%. Sequentially, the annualized headline inflation over the last quarter has been rising and sits just below 6%, while core pressures are broadly steady at an elevated 5.2%.

Our Take: While inflation came in below the BCCH’s recently updated forecasts, the sustained weakening of the CLP, real wage growth that sits above 4% (well above the 1.9% YoY 2016-2019 average), along with signaling in the MPM meeting’s minutes that validate the option of pauses in the easing cycle amid elevated uncertainty leads us to believe the Board will hold the policy rate at 5% later this month. January inflation will likely show a notable rebound (0.8-1.0%) as the downside sales event pressures unwind and electricity prices adjust further. We forecast inflation ending 2025 at 3.7%.