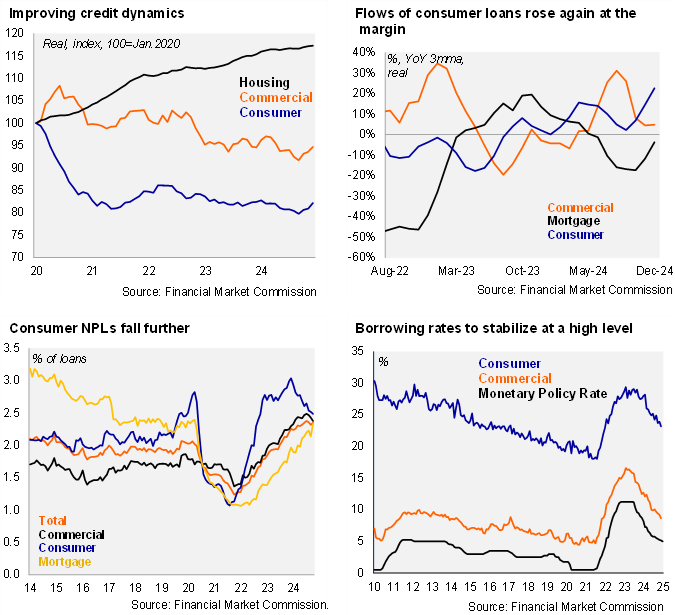

According to the Financial Market Commission, the banking system’s stock of outstanding real loans in Chile fell slightly in December by -0.34% YoY, following a decline of 0.92% in November (-1.37% in December 2023). Outstanding real commercial loans in Chile contracted again in December by 2.17%, after falling by 2.97% in November (-3.63% in December 2023), declining on an annual basis since May 2022. On a flow basis, commercial loan growth stabilized at the margin rising by an average of 4.5% YoY 3mma in real terms. Outstanding consumer loans in Chile swung back to positive territory rising by 0.16% YoY, printing positive for the first time since January 2023, after falling by 1.38% YoY in November (-2.3% in December 2023). Real outstanding mortgage loans in Chile rose by 1.68% YoY in December (1.68% YoY in November, 2.42% in December 2023).

Non-performing loans (defined as delinquencies of more than 90 days) rose slightly at the margin to 2.35% (2.32% in November, 2.13% in December 2023). The banking system’s NPLs still remain well above the March 2014 – March 2020 average of 1.95%. By loan type, consumer NPLs continue to gradually decline at the margin falling to 2.49% in December (2.52% in November, 2.89% in December 2023); consumer NPLs peaked in the cycle at 3.04% in February, with the improvement likely linked to lower borrowing costs and improvements in the real wage bill. Mortgage NPLs jumped to 2.34% from 2.14% in November, well above the 1.74% of December 2023. NPLs have creeped back up to the pre-covid 2.4% level. The rise in commercial NPLs observed in recent quarters appears to have stabilized with another slight decline in December to 2.38% (2.43% in November, 2.24% in December 2023), close to the highest level at least since 2014.

The BCCh’s 4Q24 Banking Credit Survey shows an improvement in consumer and mortgage loan demand, consistent with greater flows reported by the CMF data. According to the BCCh, the fraction of banks reporting greater consumer loan demand increased from 17 to 33%. As for housing loans, the proportion of institutions perceiving stronger demand increased from 0 to 27%. Corporate credit demand remained relatively stable at weak levels. Overall loan supply remained generally stable compared to the previous quarter, although with somewhat more restrictive conditions for housing and real estate loans as well as for construction companies. Finally, credit demand by real estate and construction companies fell again, but by a lesser extent than in previous quarters.

Monetary policy transmission is still working smoothly in the bank lending channel, as borrowing rates for commercial loans fall further. According to the BCCh, interest rates in nominal terms on commercial loans fell for the fourth consecutive month at the margin in December, averaging 8.65%, down from 9.2% in November, well below the 12.47% of December 2023; the spread with respect to the monetary policy rate fell to 3.5pp, the lowest since December 2019, and well below the two-year average (4.5pp). Rates on commercial loans are the lowest since December 2021 (8.71%). Separately, interest rates in nominal terms on consumer loans averaged 23.17% in December, down from 23.92% in November, and well below 27.58% in December 2023; the spread with respect to the monetary policy rate fell to 18.02pp, below the two-year average (18.44pp). We expect the gradual decline in borrowing rates for commercial loans to pause in the coming months, as we believe the BCCh will keep the policy rate at 5% for the rest of the year. Inflation-linked rates on mortgages fell for the fifth consecutive month to 4.37%, from 4.42% in November, and down from 5.21% in December 2023.

Our take: Loan dynamics are gradually improving, led by consumer loans. The increase in flows of consumer loans likely reflects the effects of lower borrowing costs and appears consistent with the string of better-than-expected retail sales data. Still, commercial loan dynamics have yet to signal a meaningful recovery in stalled non-mining investment, especially relevant for the monetary policy discussion in Chile. The Financial Market Commission will release bank credit data for January by the end of February.