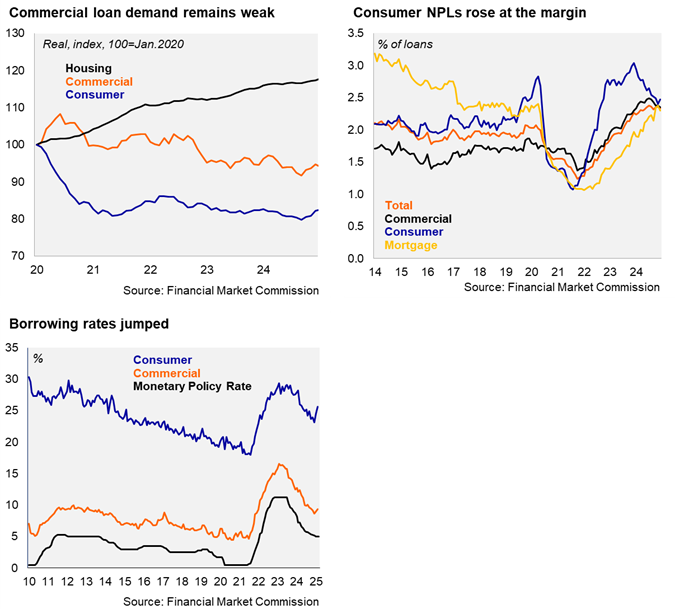

According to the Financial Market Commission, the banking system’s stock of outstanding real loans in Chile fell again in February, declining by 2.15% YoY. Outstanding real commercial loans in Chile contracted at a faster pace in February, down by 4.89% (-1.11% in February 2024), declining on an annual basis since May 2022. Outstanding consumer loans in Chile fell slightly by 0.19%, although they have been essentially flat for the past several months (-1.16% in February 2024). The stock of real outstanding mortgage loans in Chile continues to gradually decelerate, rising by 1.52% YoY in February (2.58% in February 2024).

Non-performing loans (defined as delinquencies of more than 90 days) fell slightly at the margin to 2.33% in February (2.36% in January, 2.26% in February 2024). The banking system’s NPLs still remain well above the March 2014 – March 2020 average of 1.95%. By loan type, consumer NPLs jumped 2.47% in February (2.40% in January), down from the cycle peak of 3.04% in February 2024, with the improvement likely linked to lower borrowing costs and improvements in the real wage bill. Mortgage NPLs fell to 2.3% from 2.38% in January, well above the 1.74% of December 2023, yet back up to the pre-covid 2.4% level. The rise in commercial NPLs observed in recent quarters appears to have stabilized reaching 2.35% in February (2.3% in February 2024).

Borrowing rates rose for the second consecutive month in February. According to the BCCh, interest rates in nominal terms on commercial loans rose in February to an average of 9.41%, from 8.97% in January, still well below the 12.47% of December 2023; the spread with respect to the monetary policy rate rose to 4.41pp, close to the two-year average (4.5pp). Rates on commercial loans have increased since the cycle low in December (8.65%). Separately, interest rates in nominal terms on consumer loans averaged 25.64% in February, up from 24.54% in January, and rising for the second consecutive month; the spread with respect to the monetary policy rate rose to 20.64pp, above the two-year average (18.7pp). Higher borrowing rates through the bank lending channel likely reflect shifting expectations on the policy rate path, which at the time even incorporated hikes later this year. Inflation-linked rates on mortgages also rose for the second consecutive month, to 4.45%, from 4.4% in February.

Our take: Weak commercial loan demand is a sign of concern. Commercial loan dynamics have yet to signal a meaningful recovery, suggesting the non-mining investment recovery may continue to lag. Of note, the Financial Market Regulator published their 2025-2026 regulation plan (available here), with a focus on the implementation of the consolidated debt registry law, Basel III Pillar 2, and the open finance sector, among others. The Financial Market Commission will release bank credit data for March by the end of April.