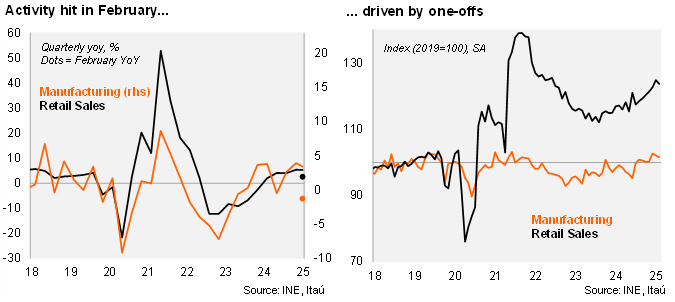

Retail sales, manufacturing and mining activity came in weak in February, mainly driven by one-offs. Mining production dropped by 0.8% MoM/SA leading to a 6.6% YoY decline (+0.5% in January), affected by lower ore-grade and site maintenance at some operations. Manufacturing fell 0.5% sequentially leading to a 1.3% YoY contraction (Itaú: -1%; Bloomberg: -1.2%; +3.6% in January). Beverage production was a key drag (-1.2pp contribution), along with paper and pulp (-0.7pp). Food processing continued to advance favorably (5.4% YoY). While retail sales were also hampered by one-offs in the month (-1% MoM/SA), annual growth still came in a respectable 2.6% YoY (Itaú: 2%; Bloomberg consensus: 2.7%; 8% in January). The continued influx of consumer tourism and an improvement at the margin of the real wage bill will likely see retail sales return to more dynamic growth ahead.

Despite the transitory setback, quarterly activity momentum remains positive. Total retail sales increased by 5.3% YoY during the February quarter (5.4% in 4Q), with durable retail sales rising 7.3% YoY and non-durable goods increasing 4.9%. Separately, total industrial production rose 2.5% in the quarter (4.4% in 4Q). Manufacturing growth came in at 3.4%, while mining rose 2.4%. In seasonally adjusted terms, retail sales increased 11.7% QoQ/saar (10.6% in 4; 0.7% in 3Q24), while manufacturing rose 7.3% QoQ/saar (2.5% in 4Q24).

Our Take: We expect February's IMACEC, to be published by the BCCH tomorrow, to rise by 0.2% YoY, down from the 2.3% in January. The more demanding base effect, due to the 2024 leap year (estimated at a 1.4pp impact on growth by the BCCh), and the partial disruption to activity during the nationwide blackout (0.5pp estimated for a full working day effect). Activity growth in March will likely return to around the 2% mark. For 2025, we have a 2.3% GDP growth forecast. Improving domestic private sentiment investment and consumption will support activity this year, while the upside pull recently experienced from the global economy may fade amid greater uncertainty over protectionist trade policies. The INE will publish March sectoral data on April 30.