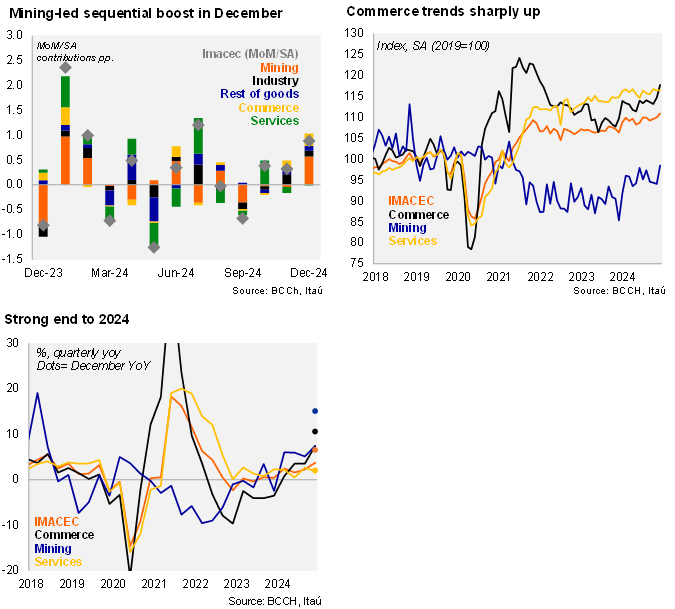

The monthly GDP proxy (IMACEC) posted widespread sequential gains in December, pulled up by the 4.7% MoM/SA mining increase, while non-mining activity rose 0.4% MoM/SA. Activity dynamics in December 2024 contrasted with the widespread sequential decline one year earlier. Overall, the economy increased 0.9% MoM/SA (-0.8% in December 2023), leading to an annual increase of 6.6% YoY, far exceeding market expectations that had a peak of 5.0% (Itaú 3.6%). The month included two additional working days and favorable base effects. Adjusting for seasonal and calendar factors, annual growth in the month was lower, but still upbeat at 4.3% YoY. Mining rose 4.7% YoY in December, while commerce ticked up 2.7%, lifted by wholesales and autos. Services rose 2% YoY. Production of cherries led to double-digit other goods production (excluding mining and manufacturing). Activity during the final quarter increased 3.7% YoY, up from 2.3% in 3Q, lifted by the 7.5% mining boom and the 7.4% commerce increase. During the full year, the economy grew 2.5%, exceeding the central bank’s 2.3% December estimate (Itaú: 2.2%).

Sequentially, the economy grew near potential during the final quarter of 2024. Activity increased 1.7% QoQ/Saar, down from 3.1% in 3Q24. Mining was broadly flat from 3Q24, while non-mining activity growth came in at 2% (3.3% in 3Q), lifted by commerce and services.

Our Take: The strong end to 2024 implies favorable carryover for 2025. If the economy were to maintain the 4Q24 levels through 2025, activity would increase by 0.6%. Mining dynamics will play a key role; after detracting from growth during seven of the last nine years, the rebound in 2024 (6.2% YoY) is welcomed. Expectations for 2025 are for the recovery to continue, with the Chilean copper commission expecting growth to persist at a 6% rate. While consumer and business sentiment remain pessimistic, they have persistently improved over the past quarters. Consumer tourism remains at play, while demand for credit is gradually improving. Imports of capital goods point to a positive investment performance this year, after two years of decline. Overall, risks are biased to the upside for our 1.9% call. Nevertheless, the uncertainty over global protectionist policies and its impact on the domestic economy may dent current growth optimism. With activity exceeding expectations, and inflation pressured to the upside in the short-term, the central bank will consolidate its messaging of staying on hold for the foreseeable future. However, the weakness of the labor market remains a key factor to monitor, as it could hold back further expansion of private consumption. The January IMACEC will be released on March 3. With the economy having started 2024 on a strong note (2.4% MoM/SA, after a weak December 2023), the more demanding base effect will likely lead to significant moderation in the annual growth figure (to around 1-2%).