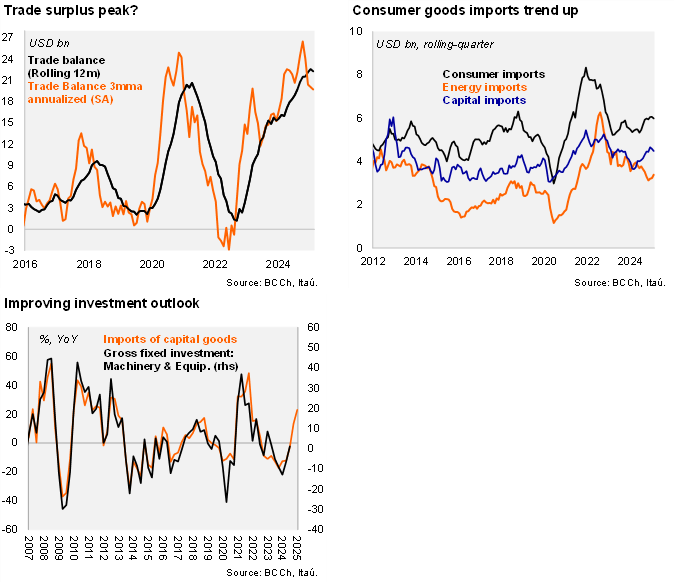

A USD 1.6 billion trade surplus was recorded in February, down USD 0.3 billion over one year. The surplus was below our USD 2.1 billion call. The rolling 12-month trade surplus reached USD 22.3 billion (similar to 2024; close to 7% of GDP; USD 15.3 billion in 2023). The annualized quarterly trade balance sits just under USD 20 billion (SA). Prior to this cycle, annual trade surpluses of around USD 20 billion were last registered in early 2021.

Annual export growth moderated. Exports rose by 0.3% YoY, down from the double-digit increases in the previous two months. Milder copper export growth and a reversal of agricultural sales (cherry exports fell 31% YoY) explain the slowdown. Lithium exports continue to shrink significantly (-61% YoY). At the margin, exports during the quarter ticked up 11% (SA, annualized; -4% in 4Q24).

Signs of recovering domestic demand consolidated. Total imports rose by 5.4% YoY (8.3% in January), lifted by the 7% rise in consumer goods imports, while capital goods increased by 24% (18% in January), signaling an expected improved ahead in private consumption and investment. Energy-related imports continued to shrink, dragged by diesel and LNG. At the margin, imports during the quarter increased 42% (SA, annualized; 17% in 4Q24).

Our Take: Even though a large trade surplus has been recorded in the first two months of 2025 (USD 5 billion, a tick above the comparable 2024 period), going forward exports are likely to reflect a moderation in the global growth outlook as imports should reflect rising domestic demand. Still, favorable terms-of-trade favor the persistence of large trade surpluses. Trade war dynamics and the effect on Chile’s main trading partners is a relevant risk to monitor. We expect the CAD to remain well-behaved at around 2.4% of GDP.