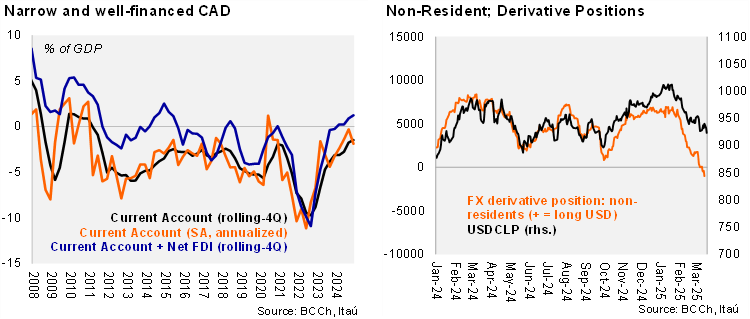

The current account deficit during 4Q24 came in at USD 1.8 billion (Itaú: USD 2.0 billion), smaller than the USD 2.7 billion deficit in 4Q23. The 4Q24 result was pressured by a large income deficit (USD 4.3 billion) as elevated copper prices likely favored FDI investment results. Nevertheless, a large trade surplus for goods and services (USD 2.5 billion; USD 1.2 billion in 4Q23) helped narrow the imbalance. As a result, the CAD during 2024 fell to 1.5% of GDP, more than half the deficit registered in 2023. The deficit is far narrower than our 2.3% estimate (BCCh: 2.4%), but the 4Q update incorporated significant revisions to the first three quarter of the year (of around +0.6% of GDP). Net foreign direct investment into Chile (around 2.8% of GDP) comfortably financed the 1.5% CAD, but during 4Q there was a net outflow of FDI (the first since 4Q23).

Our Take: A narrow CAD amid improving growth dynamics, elevated copper prices, falling inflation, the expectation of stable local rates and uncertainty regarding the US is likely supporting a more favorable external view of the CLP. In fact, the non-resident derivate position recently turned long CLP for the first time since 2022. Improving domestic demand will likely reduce the trade surplus ahead. Nevertheless, elevated copper prices and improving local sentiment will sustain investment dynamics and the healthy financing of the current account deficit. We have downside bias to our 2.4% of GDP estimate for this year.