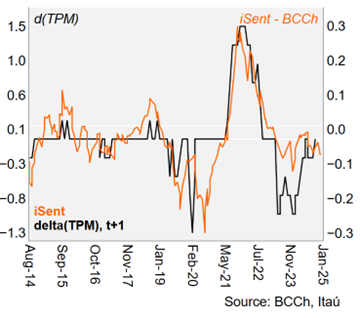

In line with the consensus and our expectation, the Board of the Central Bank of Chile unanimously decided to lower the monetary policy rate by 25bp to 5.00% in the final monetary policy decision of the year. As we had anticipated, the BCCh states that several factors have led to a more challenging short-term inflationary outlook (headline inflation to fluctuate close to 5% in the first semester of 2025) which should then moderate in the medium-term due to weaker domestic demand. While the statement recognizes that under the BCCh’s baseline scenario the monetary policy rate declines over the policy horizon, it also acknowledges that the balance of risks to inflation are biased to the upside, warranting an additional layer of caution. In fact, the guidance drops the reference of the policy rate convergence to neutral (3.5% - 4.5%).

Our Take: Easing cycle to pause, for now. We interpret the decision as a “hawkish cut” that signals the BCCh will take some time to assess if macro conditions allow for additional cuts towards the nominal neutral rate range. The Board likely discussed cutting and pausing in this meeting, which will be revealed in the minutes (January 6). Of note, following this decision, the one-year ex-ante real policy rate has fallen to 1.4%, piercing the upper bound of the BCCh's neutral real rate range (0.5-1.5%). Our baseline scenario had incorporated intermeeting cuts with a pause in January and reaching the ceiling of the nominal neutral rate range of 4.5% in June; yet the BCCh may take even longer to get there. The IPoM will be published tomorrow at 9am local time, with focus on the updated baseline scenario and corridor. The next Monetary Policy Meeting is scheduled for January 27-28.