The Central Bank’s Board unanimously kept the monetary policy rate (MPR) at 5.0% for a consecutive meeting, in line with our expectations and the market consensus. The Board noted that inflation risks remain elevated, and favor a cautious approach. As a result, the Board retained a neutral forward guidance, in line with our view of a prolonged period of rates-on-hold as further information is accumulated. The real ex ante rate, that is, discounting the one-year inflation expectation according to analysts (3.5%) from the current MPR (5.0%), sits at 1.5%, at the ceiling of the BCCh's neutral range (0.5-1.5%).

Uncertainty about the outlook for the global economy has increased significantly since January. The growth outlook for the US has adjusted down, while the inflation expectations have risen. In this context, the Fed paused its rate-cutting cycle in its recent meetings. Global financial markets movements have shown an unusual divergence. Overall, developments have led to a global weakening of the dollar, which has raised the price of some raw materials, including copper. Oil prices have corrected down amid global growth fears. Locally, credit has not shown major changes, while consumer and commercial loan interest rates continue to exhibit behavior consistent with the evolution of monetary policy.

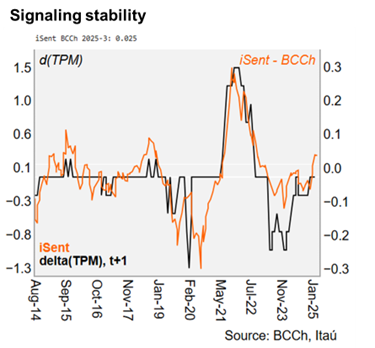

The Chilean economy has been more dynamic than previously expected, largely due the boost from exports. The improved performance of some agricultural sectors and tourism compounded growth. Both private consumption and gross fixed investment continue to gradually recover, while the labor market shows limited slack. Private sentiment has also picked up. Inflation has evolved in line with the December scenario, but the Board highlighted that some two-year inflation indicators remain above the 3% target (breakevens, trader survey).

Our Take: We believe the Board only considered the option to hold rates at this meeting. While the macroeconomic scenario has evolved broadly in line with expectations, risks (particularly to inflation) remain elevated and favor a measured approach to MP decision making. We expect the Board to hold rates at 5% this year. Our internal scenario also sees the Fed keeping rates steady in 2025. The Central Bank’s updated baseline macroeconomic scenario and rate trajectory will be published in Monday’s IPoM. We expect the new policy rate corridor to reflect a period of rates on hold, before taking further steps toward the 4% neutral nominal rate in 2026. Adopting a stay-on-hold approach in the near term will give the board time to gauge the breadth of the recent improvement in economic activity and consolidate the downward adjustment of CPI expectations, preventing a policy scenario in which the board would need to raise rates in the short term, albeit in the context of high global policy uncertainty and narrow interest rate differentials with the U.S. The minutes of the March meeting will be published on April 7.