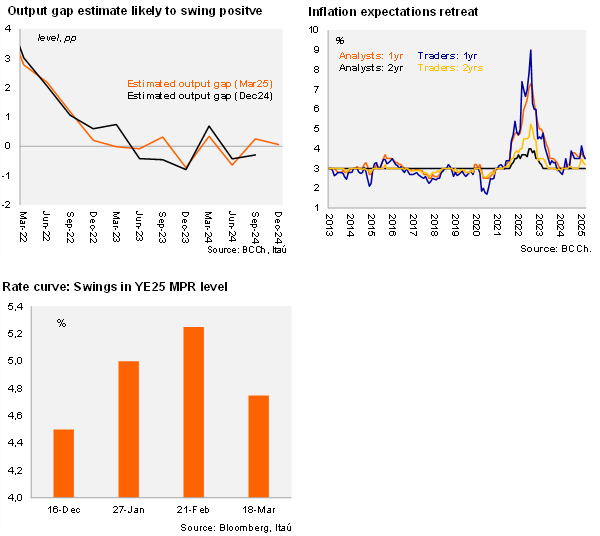

On Friday, we expect the Central Bank Board to hold the monetary policy rate (MPR) at 5% for the second consecutive month and retain a neutral bias. With the one-year ex-ante real rate already at the upper bound of the BCCh’s neutral rate range (at around 1.5%; 0.5-1.5% estimated neutral range), a likely shift to a slightly positive output gap, and elevated global policy uncertainty, we believe the bar is high for adjustments to the policy rate. We expect the new policy rate corridor, to be published on Monday with the new IPoM, to reflect a period of rates on hold, before taking further steps toward the 4% neutral nominal rate in 2026. Adopting a stay-on-hold approach in the near term will give the board time to gauge the breadth of the recent improvement in economic activity and consolidate the downward adjustment of CPI expectations, preventing a policy scenario in which the board would need to raise rates in the short term, albeit in the context of high global policy uncertainty and narrow interest rate differentials with the U.S.

Global uncertainty remains a central theme. In the January meeting, the central bank flagged developments abroad that sustained uncertainty. At the time, the uncertainty had led to a strong appreciation of the dollar and higher interest rates across all maturities, as well as tightening financial conditions globally. Since January, policy whiplash in the US and spending responses in other developed economies have resulted in a 4% weakening of the global dollar, lower long-term US rates (-25bps), and falling US activity forecasts (Itaú -0.5pp revision to 2%). The threat of tariffs on US copper imports has seen the US price spread surge, supporting a 7% appreciation of the CLP since the January meeting. While the market has priced up to three rate cuts by the Fed this year, the December IPoM considered one cut in December (similar to our internal scenario of rates on hold this year).

Activity has performed more favorably, while medium-term inflation expectations have retreated. The economy expanded by 2.6% in 2024, above the central bank’s 2.3% forecast, while growth in prior years was revised up slightly . The net effect of the activity dynamics and the improvement in leading indicators (private sentiment, capital goods imports) will likely see the central bank revise the output gap towards a slightly positive one, from negative in December, raising demand side inflationary pressures versus the December scenario. A more promising investment pipeline, gradually improving credit dynamics and the sustained period of consumer-tourism will likely lead the BCCh to raise its 2025 growth forecast range up by 50bps to 2.0-3.0%. In terms of inflation, greater demand side pressures will likely be offset by a more appreciated CLP path, resulting in only a moderate upside inflation revision. The previous IPoM forecasted a yearend 2025 CPI of 3.6% (Itaú: 4.1% with a downside bias). We expect the 1Q25 inflation average to be broadly in line with the December scenario of 4.9%. We do not expect another major electricity price hike this year, or a significant minimum wage increase (to be presented to Congress and implemented in May). High base effects in 2H are expected to support a noticeable drop in inflation. The recent CLP rally has played a key role in reverting medium-term inflation expectations. While the results of the key analyst survey never diverged from the 3% target for the two-year horizon, the share of respondents that saw greater pressure has diminished. Meanwhile, the one-year outlook dropped to 3.5%, from 3.8% in the January edition. On the trader survey front, the one-year forecast now sits at 3.5%, unwinding 65bps from the January result. The two-year vision fell 30bps since the last meeting to 3.2%. The two-year breakeven retreated from near 4% at time of the last meeting to reach 3.5%.

Our Take: Medium-term inflation expectations have declined since January, likely reflecting the swift appreciation of the exchange rate, as softer imported price pressures appear to partly offset the local cost pressure adjustment (electricity, wages). The decline in core inflation, particularly core services, and downside adjustment of inflation expectations, have chalked off previous market pressure for the central bank to raise rates as soon as 1H25. We forecast that the BCCh will keep the policy rate unchanged at 5.0% this year. We do not expect a revision to structural parameters in this IPoM.