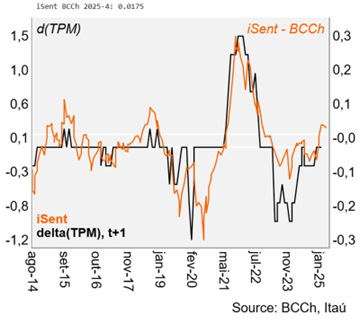

All five board members agreed that, in general terms, the development of the macroeconomic scenario had been in line with expectations during 1Q25. However, the background information pointed to an inflationary outlook that continued to face significant upside risks, reaffirming the need for caution. As a result, the Board only discussed maintaining the policy rate at 5%, for the second consecutive meeting, in line with our text indicator.

Several board members highlighted inflation risks. One central banker noted that the current level of inflation was uncomfortable in the event of potential new upward shocks, which, while potentially transitory, would occur in circumstances where inflation had been high for a prolonged period.

Sensitivity scenarios highlighted. One board member emphasized that, in a scenario where the output gap was practically closed, the most appropriate course was to maintain a message of caution regarding future policy moves and act firmly if the sensitivity scenarios materialized. In terms of shocks to the economy, some central bankers emphasized that a substantial weakening of global growth would slow activity, generating slack that could lead to a rapid decline in inflation beyond the target, which would require a looser monetary policy stance to avoid an overadjustment of the economy.

Our take: The minutes reflect an old-world scenario with much of the future strategy is likely to be linked to the materialization and magnitude of the sensitivity scenario of lower global growth. Our recent scenario saw two 25bp cuts in early 2026 to 4.5%, but the persistence of recent developments would see cuts brought forward. Today, Governor Rosanna Costa highlighted the uncertainty and that it is too early to draw definitive conclusions about the implications of the financial effects of recent days. The Governor noted that a possible outcome in the short-term may see an increase in global supply to consumers outside the United States, potentially reducing prices. In the medium term, lower activity and employment may be combined with upward price pressure stemming from the probable losses in efficiency at the global level. The next monetary policy meeting takes place on April 28-29.