The Board agreed that holding rates at 5% was the only plausible option in January. Several board members signaled that the decision was coherent with prior signaling that pauses amid elevated uncertainty were a possibility. In turn, the decision provides time to accumulate more information and reevaluate the policy strategy that is consistent with achieving the targeted inflation convergence path. Amid rising inflation expectations, several Board members stressed the need to emphasize concern about the evolution of two-year inflation expectations, reaffirming that the BCCh was prepared to act if meeting the inflation target was deemed at risk. One Board member was specific in mentioning the use of hikes if necessary. The December IPoM signaled an average policy rate of around 4.25% during 4Q25, but improved activity and elevated inflation will likely lead the March scenario update to reflect a rate path with no changes this year (that is, stable at 5% nominal). A CLP appreciation since the January meeting (3.5%; 4.6% over one-month) and a drop in the share of surveyed respondents seeing higher two-year CPI will likely provide the Board with some breathing room to keep rates steady going forward. Nevertheless, upcoming EEE survey results (March 11) will be eagerly awaited by market participants to see if a hiking reaction is eventually triggered.

On the external front, the scenario continued to be dominated by economic uncertainty and geopolitical tensions. The Fed’s tone had become more contractionary, as activity continued to surprise positively. Domestically, the macroeconomic scenario was broadly in line with the December IPoM. Although inflation closed 2024 somewhat below the internal forecast, trend indicators remained generally to the upside, and velocities were still above those consistent with the target. Short-term forecasts continued to reflect inflation around 5% during the initial phase of the year. The activity and labor market gaps were narrow. Imacec prints had been greater-than-expected, although influenced by one-off factors, while the seasonally adjusted unemployment rate remained at around 8.5%. Commercial credit reflected a slight rebound at the margin, but insufficient to clearly indicate a change in trend.

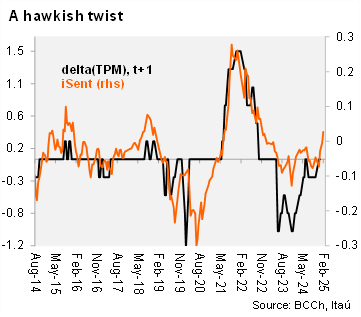

The evolution of two-year inflation expectations was the key focus of the meeting. Although the median response in the Economic Expectations Survey (EEE; analysts) remained at the 3% target, a significant fraction (42%) believed that inflation would be higher. Meanwhile, the Financial Traders Survey (EoF) showed that two-year inflation expectations would be above target. Financial asset prices (even when considering known distortions), also pointed to estimates above the target. The Board considered it premature to establish whether the evolution of the two-year CPI outlook would have an impact in inflationary persistence, but it was a warning sign that could not be ignored. The Board recalled previous instances when expectations surged, resulting in the need to aggressively respond on the monetary policy front, further denting economic dynamics. Since the January meeting, a new EEE survey was released showing the fraction of respondents seeing above 3% inflation dropped from 42% to 33%. On Friday, a new EoF survey will be published.

Our Take: The BCCh board showed their teeth and willingness to do “whatever it takes.” The Minutes confirmed our expectation that holding rates was the only option considered in January, while the hawkish communication will likely eliminate expectations of further cuts this year (still incorporated in the EEE and EoF surveys). With ex-ante real rates already around neutral levels, we believe staying on a more cautious path (no rate cuts this year versus the near 4% YE signaled in the December IPoM) is the most beneficial in terms of consolidating an inflation convergence path towards the 3% over the policy horizon. While not our base case, we cannot discard the next move being a hike if inflation expectations deteriorate. Nevertheless, we still see most of CPI pressures stemming from transitory supply adjustments that will likely begin normalizing during 2H25 and soften medium-term expectations.