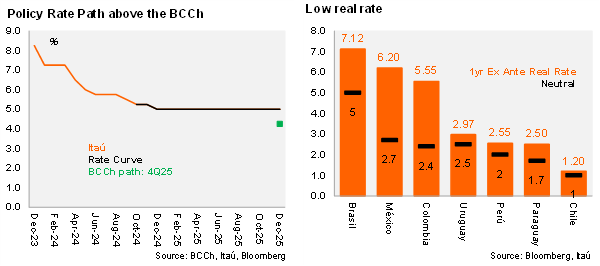

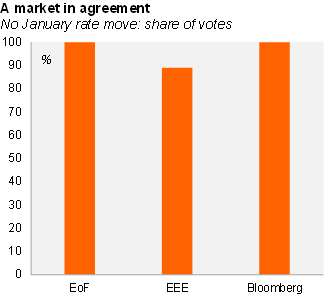

The central bank has guided the market towards a stay-on-hold decision at its January monetary policy meeting (28th). Even though inflation surprised to the downside in December, short-term domestic inflation is being pressured to the upside, mainly due to supply factors, while there is significant global uncertainty on the effects of shifts in economic and trade policies in the US on inflation and activity. Under such uneasy circumstances and considering that the policy rate in real ex-ante terms (1.2%) is already in the upper bound of the neutral rate range (0.5-1.5%), the most logical response is to pause the cycle, gather additional information and re-evaluate the baseline scenario along with the appropriate rate path at the March IPoM (decision on March 21, IPoM on March 24). While we no longer see room for rate cuts this year, we lean towards the central bank continuing to signal softer demand-side inflationary pressures in the medium-term that would support rates below their current levels over the two-year policy horizon.

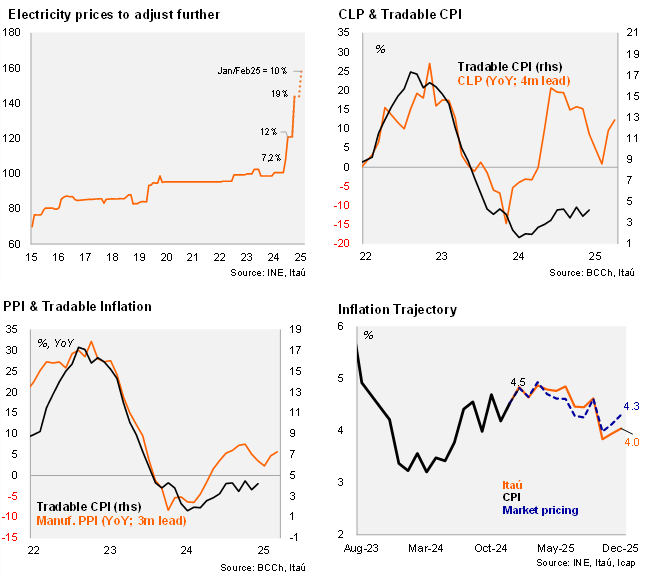

A strong dollar brings greater short-term inflation fear. The local economy remains weak, evidenced by slack in the labor market and a slightly negative output gap, but with the CLP roughly 10% weaker than at the start of 2024, tradable price pressures will persist. Additionally, another large electricity price increase is set for the start of the year (+10%, 2.2% of the CPI basket), while general indexation mechanisms will add a further layer of price adjustments. We expect inflation of 4% this year (IPoM: 3.6%; 4.5% in 2024), a fifth year of above-target inflation.

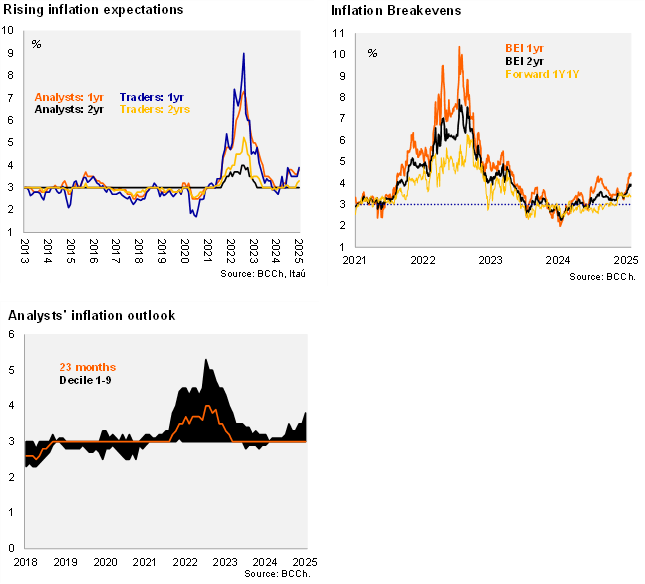

Rising medium-term inflation expectations are a sign of concern. While supply factors are clearly behind the higher short-term expectations, rising medium-term expectations amid the lack of domestic growth drivers is a warning sign that is sufficient justification to hold rates for the time-being.

The scenario requires more caution. We expect the central bank to highlight the markets’ expectations of a US interest rate trajectory that has become even less expansionary; notably, the December IPoM incorporated a total of three 25bp cuts in 2025. Oil prices have also been above the December IPoM’s forecast (Brent spot: USD 79/barrel; IPoM annual average: USD 71). On the domestic front, the Board will likely reinforce the upwardly biased balance of risks for inflation in the near term. Signaling a period of steady rates at 5% until there are clearer signs of fading inflationary pressures will meet market expectations and avoid an adverse financial market reaction. As one-year inflation expectations have increased since the last meeting by 20-60bps (to 3.8-4.2%), depending on the survey or curve, the one-year ex-ante real rate is much closer to the 1% neutral level, providing a further reason to embark on a period of stability.