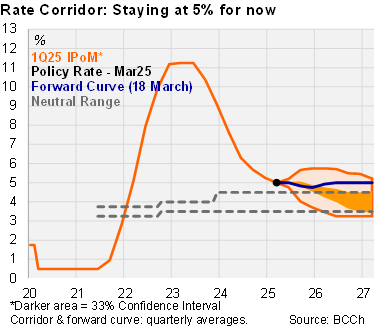

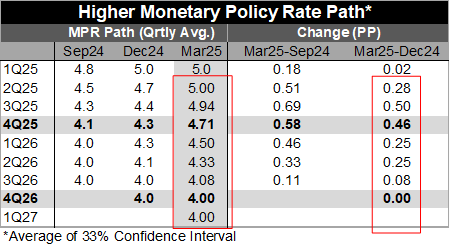

The central bank’s 1Q monetary policy report (IPoM) had few changes to the macro scenario, but elevated uncertainty favors a more cautious policy rate path. The rate corridor shows an average nominal rate that is 50bps higher during 2H25 compared to the 4Q24 IPoM. The 4.7% average for the nominal policy rate seen in 4Q25 is consistent with the policy rate ending the year at 4.5%. The end point of the cycle remains at the center of the BCCh's neutral nominal range of 4%, but only reached by late 3Q26, about a quarter later than in the previous scenario. We expect rates to stay on hold for 2025, but if conditions permit, the BCCh would favor cutting rates during 2H25.

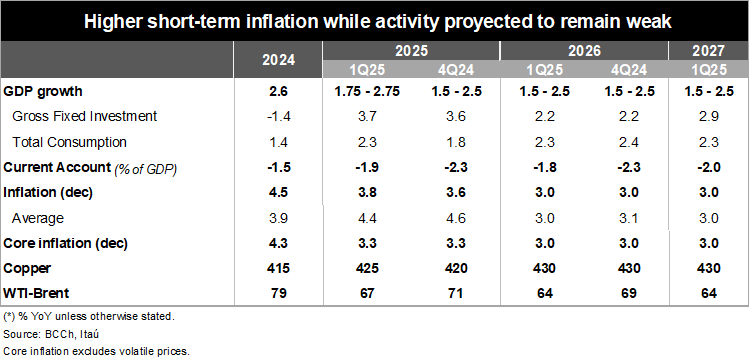

Deterioration of the external environment is seen having a limited effect on local activity. The scenario sees lower growth for trading partners, especially in 2026, amid protectionist trade policies. The largest correction is seen in the United States, with 2026 growth now estimated at 1.5% (from 2.2% in the 4Q24 scenario). However, if risk scenarios materialize, their effects would be greater, depending on how the transmission channels behave in both the trade and financial spheres. In terms of monetary policy, the scenario update incorporates fewer rate cuts by the Fed this year (2x25bps; 3 cuts in the Dec24 edition). This has occurred amid a slowdown in the inflation convergence process in recent months. Commodity forecasts remain broadly unchanged from the previous scenario, except for a downward correction in fuel prices (due to lower global demand). As a result, the terms of trade are seen above levels estimated in December and support the CAD remaining at a low 1.9% of GDP this year (-1.5% in 2024).

Improved domestic growth outlook. Limited slack in the labor market, a rebound in consumer expectations, and the real appreciation of the peso supports a greater private consumption outlook for this year (2% vs 1.6% previously). At the margin, high-frequency indicators such as trade and imports of consumer goods (partly influenced by non-resident spending) are trending up. The forecast for gross fixed investment is broadly unchanged but there still are differences across components and sectors. The 3.7% investment increase (-1.4% in 2024) will be led by mining and energy, with more limited growth in other non-mining sectors. Overall, the output gap is estimated to remain around equilibrium over the coming quarters (from somewhat negative in the previous scenario). Improved activity dynamics, boosted in part by exports, led to a higher growth scenario for this year (1.75-2.75%, +25bps). The configuration of risks to domestic activity and spending has been evolving with a reduced likelihood of less favorable internal forces and their negative effects on the local economy. Yet, the possibility of more disruptive global events and their economic and financial impacts are relevant.

Inflation is still seen converging to the 3% target by early 2026. This scenario considers the recent real exchange rate appreciation, the lower outlook for global energy prices, and the dissipation of the cost shocks the economy faced in late 2024 and early 2025. The central scenario assumes that the RER will remain around current levels for the forecast horizon (we estimate at 101). The improved outlook for domestic demand counters part of the downward adjustments. Headline inflation is expected to average 4.6% during 2Q25, after reaching around 5% during the first quarter of this year. By the end of the year, inflation is seen at 3.8% (3.6% previously) and to hover around 3% in the first quarter of 2026. Core inflation is unchanged at 3.3% by yearend. Average headline inflation is seen somewhat lower this year. The swift inflation decline outlined during 2H25 and 1Q26 is significantly influenced by the high comparison bases created by the electricity rate hikes that occurred between the second half of last year and the beginning of 2025.

Unusually elevated global policy uncertainty favors a cautious monetary policy strategy. The rise in cost pressures in recent months poses upside inflation risks, while the CLP appreciation and lower fuel prices plays a counter role. The baseline policy rate trajectory signals rates remaining on hold during 2Q25, before cuts resume during 2H25. The rate corridor shows an average rate that, in nominal terms, is 50bps higher during 2H25 compared to the 4Q24 IPoM. The 4.7% average seen in 4Q25 is consistent with the policy rate ending the year at 4.5%. Regarding the rate corridor’s sensitivity scenarios shows that high and sticky inflation, linked to greater domestic demand and higher rates of price passthrough (particularly given compressed operating margins for business). The upper bound of the corridor signals rates averaging 5.75% in 4Q25. On the other hand, rates would need to be cut faster if a scenario of tariff measures and greater global uncertainty is accentuated, denting private sentiment and spending and diminishing inflation pressures. Rates would average 3.7% in 4Q25 under softer demand circumstances. The BCCh’s baseline scenario sees a limited domestic impact, for now, from the changing global outlook.

Our Take: With the real ex ante rate, that is, discounting the one-year inflation expectation according to analysts (3.5%) from the current MPR (5.0%), sitting at the ceiling of the BCCh's neutral range (0.5-1.5%), the Board has time to spare, accumulate more inflation and gauge the breadth of the recent improvement in economic activity and the CPI trajectory. Global risks remain high, with the impact on the local economy far from clear. We expect the Board to hold rates at 5% this year, before resuming cuts to 4.5% early next year. Our internal scenario also sees the Fed keeping rates steady in 2025. Nevertheless, a scenario where the output gap remains broadly in equilibrium and the inflation convergence accelerates during the latter part of the year may lead the BCCh Board to resume easing policy ahead of schedule. We see the balance of risks tilting towards earlier rate cuts than hiking rates before yearend. The minutes of the March meeting will be published on April 7.