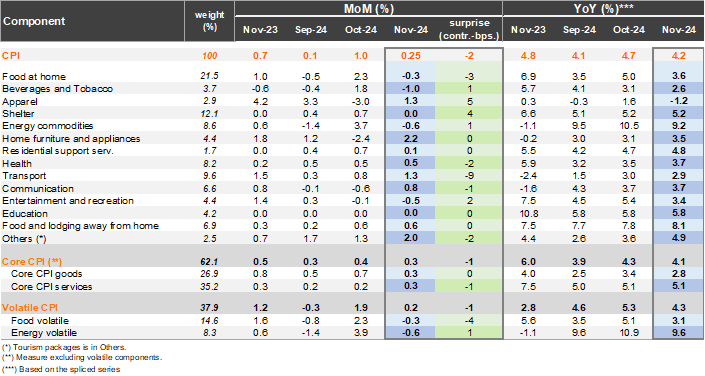

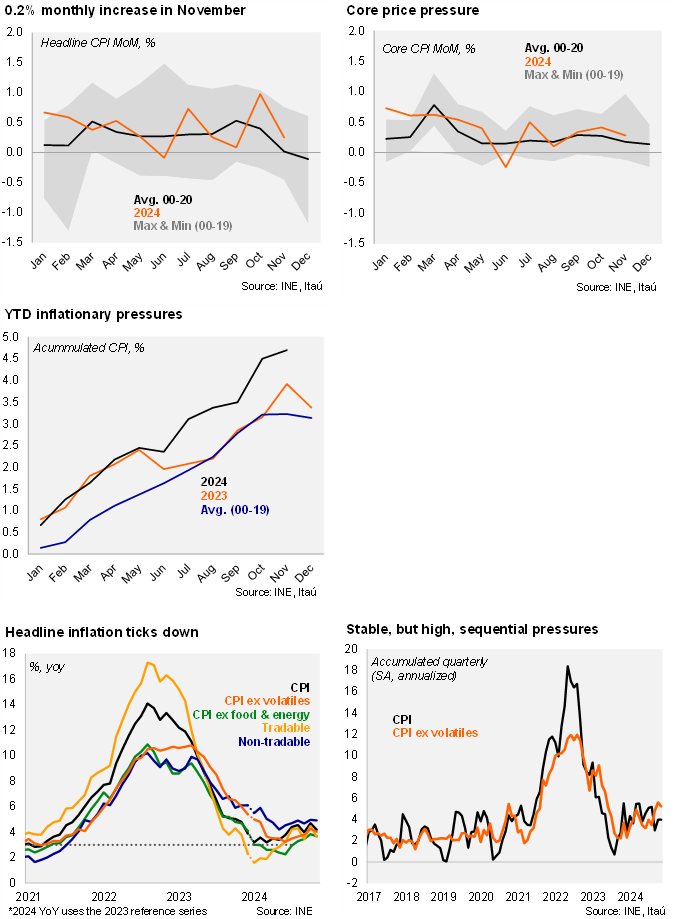

Consumer prices rose 0.2% (0.25%) from October, in line with our 0.23% call, while a tick below the 0.3% Bloomberg consensus. The key drivers in the month came from the household goods and maintenance division (9bps), communication (5bps, computers), and apparel (4bps), reflecting payback from the previous month’s sales events. The food and beverage division showed a moderate decline from October. Ex-volatile inflation rose 0.3%, also close to our monthly projection of 0.26%. Following the large October CPI surprise, second-round effects in this print seem to have been contained in November, although risks remain for coming months from the rise in electricity prices and the significant minimum wage increase, among others. In parallel, the depreciation of the peso has been persistent. Inflation accumulated in the year through November sits at 4.7%.

Core inflation pressures remain high, but soft domestic demand suggests they are unlikely to linger for long. Annual variation sits at 4.2% (down from 4.7% in October). Core inflation also sits at 4.0% (4.3% previously). Core goods and core services both rose 0.3% MoM, leading respective annual variations of 2.7% (-50bps from October) and 5.0% (-10bps). Volatiles rose by 0.2% MoM, dragged down by declines in food and energy prices, and leading to an annual increase of 4.4% (-100bps). Sequentially, the annualized headline inflation over the last quarter sits at 4%, while core pressures are higher at 5.2%, but have dropped from 5.6% in the previous month.

Our Take: The effect of renewed sales events at the backend of November and early December could see risks tilted towards a negative print for December (January 8, we provisionally estimate 0%; 4.7% YoY). The recent CLP developments, if maintained, will sustain higher core goods prices in the near-term, and prevent a swifter CPI correction in 2025. Another large electricity price hike (+7% MoM) is penciled in for January. Nevertheless, on the activity front, there are limited signs to believe demand-side inflationary pressures are consistent with a sustained above-target CPI. Employment levels have been roughly stagnant over the last semester, real wage growth is slowing, credit dynamics have yet to respond despite strong transmission to rates. The copper price drop may dent the improved investment signals that we had seen at the margin. Business surveys show limited room to transfer higher cost pressures to final consumer prices. In all, the slow convergence to the target is mainly supply related, along with the second-round effects (albeit limited so far). We don’t expect major changes to the policy rate corridor in the upcoming IPoM, but the forward curve, and market expectations will likely consolidate around the upper bound of the neutral rate range (4.5%), rather than the signaled 4% center point. In this context, we expect the BCCh to maintain its strategy of gradually reducing the policy rate towards neutral with a 25bp cut to 5% in December and continue to 4.5% in June 2025.