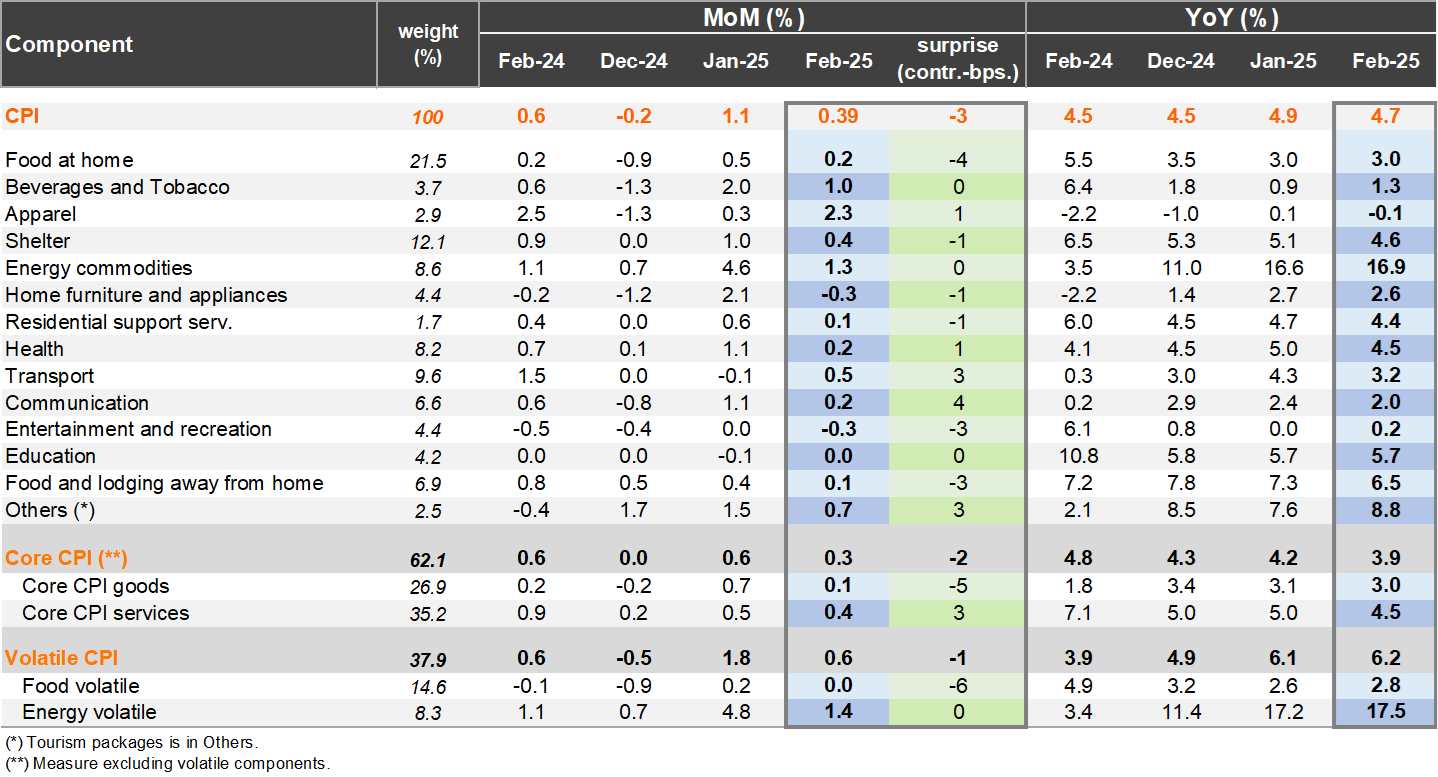

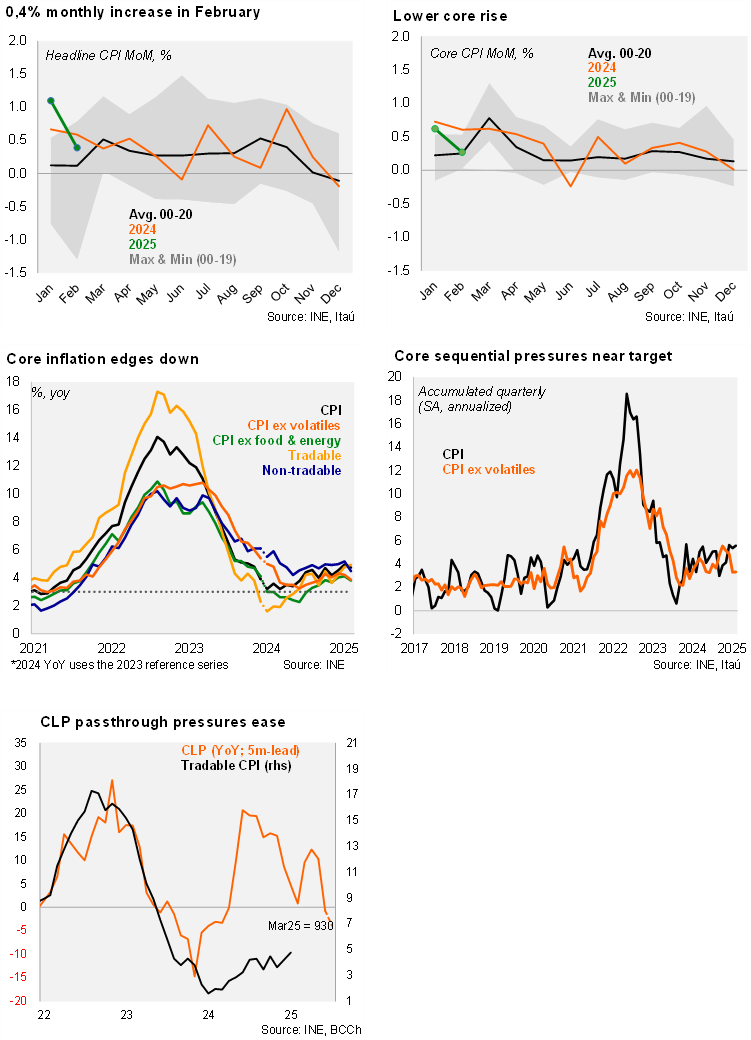

The CPI increase of 0.39% from January to February was in line with our call (also the Bloomberg consensus and implicit in the curve). The price pull was led by the transport division rising 1% MoM, pulled up by gasoline (contributing 7.5bps), and interurban transportation (+3bps). The housing division rose by 0.5% MoM, contributing 9bps, lifted by rent (responding to prior inflation) and gas. Core prices (excluding volatile items) increased 0.3% from January (Itaú: 0.3%). Second round effects from the prior electricity adjustments remain contained.

Core inflation dynamics are better behaved. In annual terms, headline inflation ticked down 20bps to 4.7%. Annual inflation has been above the 3% target since early 2021. Core inflation reached ticked down 30bps to 3.9%, the lowest rate since September last year. Core goods inflation rose 0.1% MoM and 3.0% YoY% (3.1% in January), while core services dipped 50bps to 4.5%, the lowest core service print in more than three years. Volatiles rose 0.6% MoM, leading to an annual increase of 6.2%. Sequentially, the annualized headline inflation over the last quarter reached 5.6%, in line with 4Q24, while core pressures came in at near-target 3.3% from a recent 5.5% peak in the October ’24 quarter.

Our Take: The decline in core inflation, particularly core services, along with the recent CLP rally and downside adjustment to inflation expectations will likely lay off prior market pressure that the central bank would hike rates as soon as 1H25. We forecast the BCCh to keep the policy rate unchanged at 5.0% this year. We preliminary expect a March CPI (to be published April 8) of 0.5-0.6%, driven by educational price adjustments (6%), and see a YE rate of 4.1%, with core inflation closer to 3.5%.