In the first Monetary Policy Meeting of the year, the Central Bank’s Board unanimously kept the monetary policy rate (MPR) at 5.0%, in line with our expectations and the broad market consensus. The pause occurs after the 25bp cut in the December meeting. More importantly, with greater short-term upside inflation risks, the Board’s forward guidance moved to neutral, in line with our view of a prolonged period of rates-on-hold as further information is accumulated. The real ex ante rate, that is, discounting the one-year inflation expectation according to analysts (3.8%) from the current MPR (5.0%), remained at 1.2%, within the BCCh's neutral range (0.5-1.5%).

The statement confirms that inflation projections remain biased upwards in the short term, while local activity has performed somewhat better than anticipated. On the external front, high levels of uncertainty, fewer cuts by the Fed, and the rise in oil prices, among other factors, were highlighted.

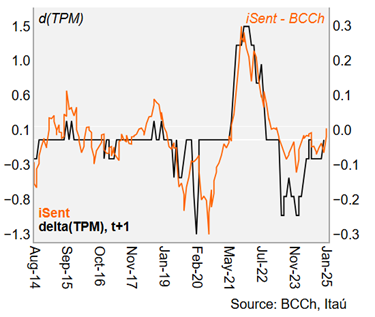

In contrast to the previous statement, the Board eliminated the signaling of further cuts, consistent with the higher short-term inflation risks and the rise in medium-term inflation expectations.

Our Take: The neutral bias favors a period of accumulating data to better understand the drivers of medium-term inflationary pressures. We believe that the Board only discussed holding the policy rate at this meeting (to be confirmed in the respective minutes on February 12). With global uncertainty likely to be sustained this year and supply-side pressure set to keep inflation high, we do not see room for rate cuts this year. We expect the BCCh to maintain the policy rate at 5.0% for the rest of the year. We estimate that inflation will close 2025 at 4.0% (BCCh: 3.6%), and for the economy to grow by around 2% this year (in line with the BCCH's projected range of 1.5-2.5%). We still lean towards the central bank continuing to signal softer demand-side inflationary pressures in the medium-term would support rates below their current levels over the two-year policy horizon. The next meeting will be on March 21 (IPoM on March 24).