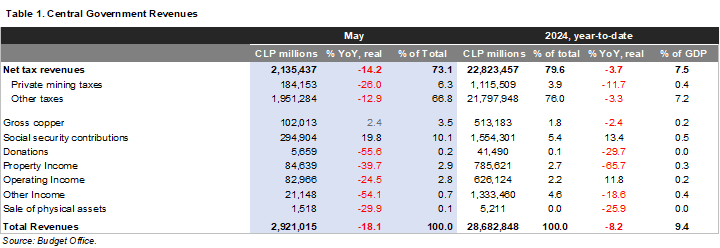

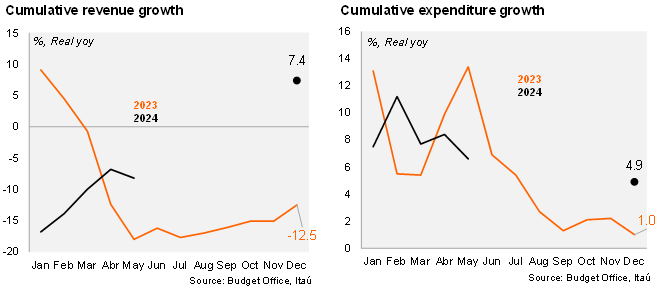

Revenues nose-dived in May, falling by 18.1% YoY, interrupting the string of improvements of previous months, and posing risks to the MoF’s ambitious annual revenue forecast. The decline in May was mainly driven by large tax returns in the aftermath of April’s tax season, which led cyclically sensitive revenues (tributación resto contribuyentes) to fall by 14.2% YoY and private mining revenues by 26% YoY. Property rents, mainly related to lithium payments from CORFO, plummeted by 39.7% YoY, reflecting lower lithium prices. In contrast, CODELCO’s payouts rose by 2.4% YoY. More details on revenues are available in Table 1. Revenue growth remains well below target, as we estimate that the shortfall in cyclically related revenues (tributación resto contribuyentes, 79% of total 2024 forecasted revenues) through May is equivalent to roughly 4% of the official forecast. Altogether, real revenues as of May have declined by 8.2% YoY (-6.8% as of March), implying a significant improvement would be needed to achieve the +7.4% official 2024 forecast.

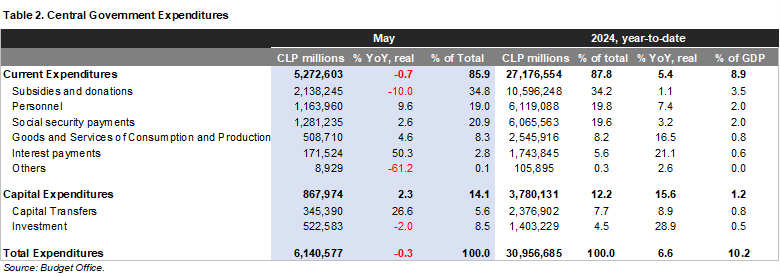

Spending growth contracted in the month, after a very strong start to the year. The central government’s real expenditures fell slightly in May by 0.3% (+8.4% YTD through April). Current expenditures declined by 0.7% YoY in May (+7% YTD through April), mainly due to base effects in subsidies and donations (-10% YoY), although spending in personnel marches on, increasing by 9.6% YoY, directionally consistent with the increase in public employees as reflected by INE’s labor market survey. Interest payments shot up by 50.3% YoY in real terms. Capital expenditures growth moderated again, rising by 2.3% YoY, down from 4.8% YoY in April, with a 9.6% YoY increase in investment contrasting with a second consecutive contraction in capital transfers to regions (-2% YoY). Spending growth in the year through May has increased by 6.6% YoY, down from the 8.4% in April, still above the MoF’s 2024 projected 4.9% YoY rise. More details available in Table 2.

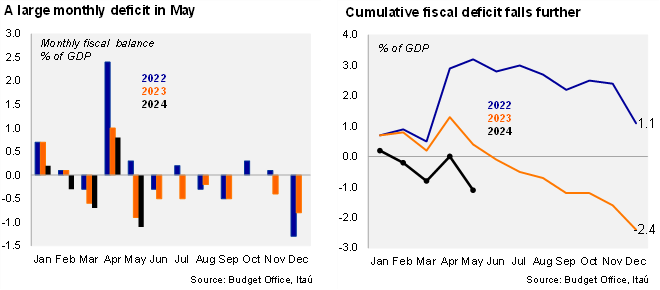

The cumulative fiscal balance deteriorated in May, as expected. The monthly fiscal balance in May snapped back to a deficit of 1.1% of GDP (+0.8% of GDP in April), slightly larger than the 0.9% of GDP deficit of May 2023. The year-to-date fiscal balance now reaches -1.1% of GDP (0.4% YTD as of May 2023). The MoF’s 2024 nominal (structural) fiscal balance forecast is 1.9% (2.2%) of GDP, implying a moderate fiscal consolidation from the 2.4% of GDP and 2.7% of GDP nominal and structural deficits in 2023. Gross public debt reached 40.7% of GDP by the end of 1Q24, and the MoF projects 40.6% of GDP by the end of 2024.

12-month rolling fiscal deficit widened further. On a 12-month moving average as of the end of May, the central government’s revenues reached 21.5% of GDP, and expenditures 25.2% of GDP, leading to a cumulative deficit of 3.8% of GDP, well above the annual cumulative deficit of 1.7% reached in May 2023, reflecting the fiscal deterioration throughout the course of this cyclical adjustment.

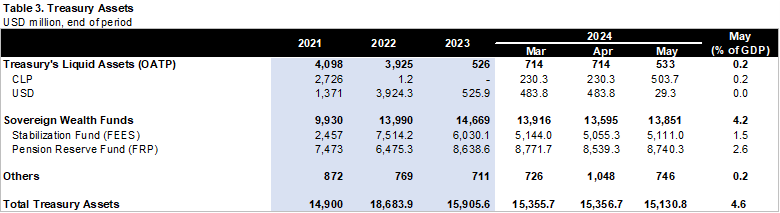

“No hay plata.” According to the Budget Office’s Monthly Asset Report, the Treasury’s liquid assets by the end of May fell to USD533 million, down from roughly USD 1 billion by the end of April (see Table 3). By the end of May, USD503 million were denominated in CLP assets, and the remaining USD29 million in dollar-denominated assets. No withdrawals nor injections to the Sovereign Wealth Funds were reported in May, leading the Stabilization Fund (USD5.1 billion) and the Pension Reserve Fund (USD8.7 billion) to have marginal valuation changes in the month. In any case, we expect the June report to include a withdrawal from the Stabilization Fund for USD 607 million, taken out to finance the annual injection to the Pension Reserve Fund (0.2% of GDP), and a withdrawal of 0.1% of GDP from the Pension Reserve Fund.

The MoF resumed dollar sales in June, as expected. As had been anticipated by the MoF, dollar sales resumed in June at a weekly maximum of USD200 million, reaching USD 792 million in the month, and a total of USD2.712 billion in the year. As mentioned earlier, the MoF had a total of USD29 million in liquid dollar denominated assets by the end of May, so sales in the month must have been financed from copper-related revenues (likely USD400 million), and dollar inflows from USD500 million from dollar inflows related to the end-May local currency issuance (in which offshore accounts paid for local currency bonds in USD). Dollar sales in July are likely to be sourced from the Pension Fund Withdrawal for USD307 million and inflows from copper related revenues, which put together would likely be below the USD 200 million maximum weekly guidance. However, new offshore issuances from the sovereign could lead to large dollar inflows. The MoF's dollar sales finance shortfalls in the central government's deficit, with expenditures are primarily in CLP. We expect the MoF to sell a total of USD6 billion this year, below 2023’s USD12.2 billion, yet eventual changes in the currency composition of the MoF’s financing could lead to greater dollar sales.

Our take: While the revenue slump in May is likely transitory, due to the large post-April tax returns, we still believe that the revenue forecast seems ambitious, which should lead to spending contractions in the near term to comply with this year’s structural deficit target. Revenues should eventually pick up reflecting the recovery of economic activity and elevated copper prices. Separately, considering the combination of low liquid balances with monthly deficits at this time of the year, low demand in recent local currency bond auctions through the Central Bank’s auction system (SOMA), and the fact that the MoF has not yet announced their 3Q24 local currency issuance calendar, we would not be surprised if the MoF had to issue more debt offshore in July. More information on Chile’s fiscal dynamics is available in this report. The June monthly fiscal report is scheduled for July 31.