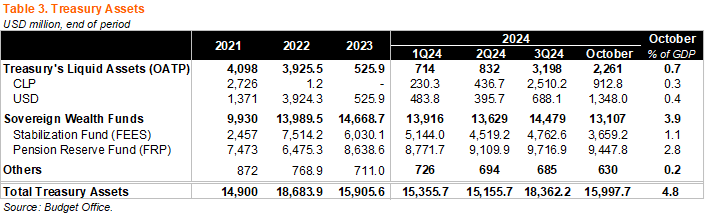

Revenues turning the page... The title of last month’s fiscal note (“Starting to shake off the revenue gloom?”) highlighted the revenue recovery in recent months. Data from October adds further evidence that the persistent revenue weakness that has haunted fiscal accounts this year may have finally turned the corner, with real revenues rising by 14.8% YoY in October (11% in September). All revenue components printed positive, with the sole exception of lithium-related property rents. Importantly, cyclically related revenues rose by a whopping 22% YoY (see Table 1 below). Despite the improvement in the month, cumulative revenue growth in the year rose at the margin to -1.2% YoY (-2.9% through September), still well below the MoF’s annual revenue growth forecast (+5.3%), suggesting the recovery may be too little, too late.

Spending jumped in October, led by a 103% YoY rise in interest payments. Real fiscal expenditures rose by 11.8% YoY in October, driven by sizable increases across both components (see Table 2 below). Current expenditure growth rose by 12.1% YoY, mainly driven by greater interest payments but also increases in personnel, and subsidies and donations. Capital expenditures rose by 10.2% YoY. Cumulative expenditure growth in the year reached 6.1% (5.5% through August), implying a material spending constraint would have to be implemented through year-end to comply with the MoF’s spending growth forecast of 3.5%.

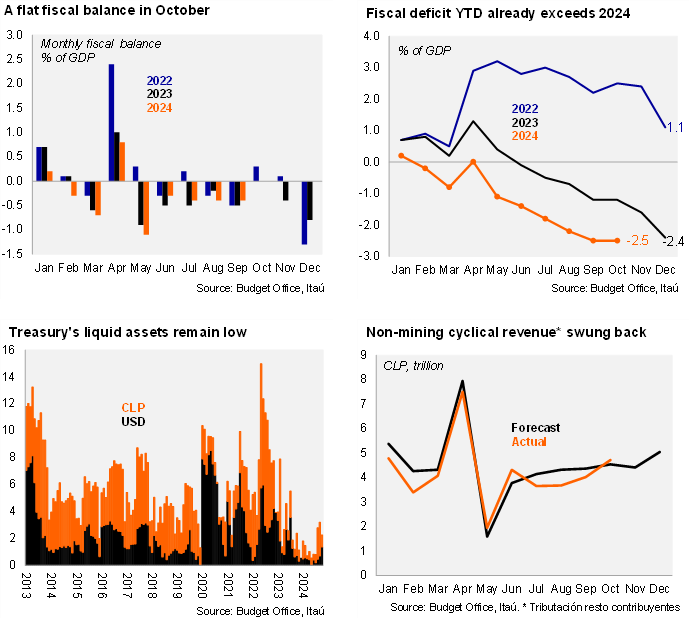

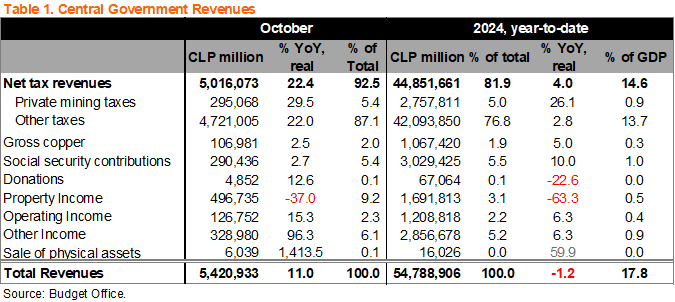

The cumulative fiscal deficit in the year through October remained at 2.5% of GDP, exceeding the MoF’s 2.0% year-end nominal deficit forecast and last year’s annual deficit (2.4%). The monthly fiscal balance in October was flat at 0.0% of GDP, equivalent to the monthly balance of October 2023. The year-to-date fiscal balance now reaches -2.5% of GDP (-1.2% YTD as of October 2023), diving well below the MoF’s annual nominal deficit target of 2.0% of GDP. The fiscal balance tends to deteriorate during the fourth quarter of every year, with 4Q23 accumulating a whopping deficit of 1.2% of GDP, suggesting the MoF will miss its nominal forecast even with a significant spending restraint.

12-month rolling fiscal deficit flat at the margin at 3.7% of GDP. On a 12-month moving average basis as of the end of October, the central government’s revenues reached 21.7% of GDP, and expenditures 25.4% of GDP, leading to a cumulative deficit of 3.7% of GDP, unchanged from the previous month (-2.6% of GDP in October 2023).

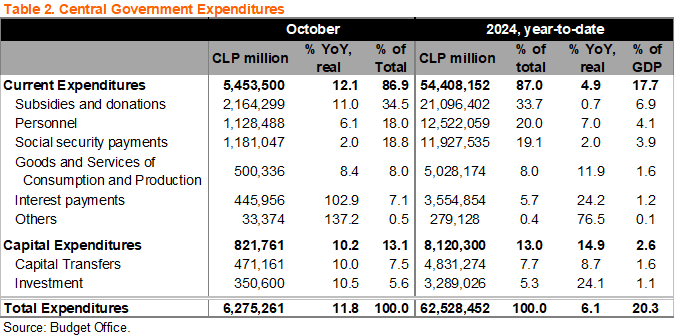

2024 debt issuance plan cut short in November, even as liquid assets remain very low. According to the Budget Office’s Monthly Asset Report, the Treasury’s liquid assets by the end of October fell to USD2.3 billion (USD3.2 billion by the end of September), the lowest level for the end of the month October at least since 2010. The decline at the margin in CLP denominated liquid assets likely reflects regular financing needs and amortization of notes towards the end of the month. Nonetheless, the MoF’s DMO announced on November 26 that it had completed the local currency bond auctions for the year, suspending two auctions scheduled for December (nominal bonds maturing in 2056 and inflation-linked bonds maturing in 2055) for a total of USD190 million, according to our estimates. The announcement came as a surprise considering these dates were added to the 4Q24 calendar only about a month prior (October 18), in the context of persistent revenue underperformance leading to low liquid assets at the Treasury as the fiscal deficit seasonally balloons.

Assets in the Stabilization Fund fall to the lowest level since December 2021. Assets in the sovereign wealth funds fell in the month mainly reflecting the USD 1 billion withdrawal from the Stabilization Fund. The Stabilization Fund (FEES) fell from USD4.76 billion in September to USD3.7 billion, the lowest since December 2021 (USD2.5 billion, prior to the last savings contribution of USD6 billion). The Pension Reserve Fund (FRP) fell to USD9.4 billion, from USD9.7 billion in September. No withdrawals nor contributions are expected from/to either fund through yearend.

Dollar sales to continue at least through mid-December. On November 13, the MoF announced that the weekly maximum cap on dollar sales would increase from USD 200 million to USD 400 million. In our view, the announcement was driven by the accumulation of liquid dollar holdings at the Treasury, the sizable seasonal 4Q deficit, and important amortizations of local currency notes due by the end of November (USD 1.8 billion). Even though the MoF has tended to sell well below the cap of their guidance throughout most of the year, a deeper look at the details suggest they are likely to sell their USD400 million weekly cap at least through mid-December. As we anticipated (here), the MoF’s dollar denominated liquid assets reached USD1.35 billion by the end of October (we had forecasted USD1.4 billion), essentially equivalent to dollar sales in November. The MoF should continue selling the USD400 million weekly maximum cap at least through mid-December, sourced primarily from mining related revenues in dollars. The MoF's dollar sales finance shortfalls in the central government's deficit, with expenditures primarily in CLP, and do not target a given level of the exchange rate.

Our take: MoF still set to miss this year’s fiscal deficit forecast. Revenue dynamics are improving at the margin yet should be too little too late, while spending cut announcements are not yet clear in the data. At 2.5% of GDP by the end of October, the year-end nominal deficit is likely to end the year close to our 3.0% projection, well above the MoF’s 2.0% forecast. The structural deficit target of 1.9% of GDP is also likely to be missed, eroding the credibility of the fiscal institutional framework. On the financing side, dollar sales should continue through mid-December, and debt issuance in international markets should resume during the second half of January 2025. Details on the MoF’s pilot market-maker’s program have yet to be announced, while the MoF also mentioned they would update their macro forecasts after the 3Q24 National Accounts (November 18). The next monthly fiscal report (November) is scheduled for December 30.