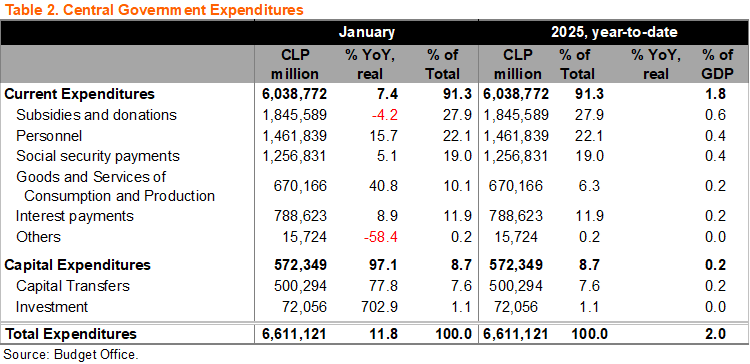

The good … revenues outperformed in January. As we’ve anticipated for several months, revenues continue to gradually improve, rising by 9.6% YoY in real terms in January. The improvement was, again, driven mainly by cyclical factors and mining (also base effects due to the implementation of the revised royalty law, see Table 1). On a positive note, non-mining cyclically related revenues, which account for roughly 74% of the MoF’s annual revenues, were somewhat above our forecast (see chart). The revenue jumpstart to the year, above the MoF’s annual 8.0% forecast, contrasts with last year’s dynamics in which real revenues rose by 1.0%, significantly below the MoF’s 5.3% forecast.

The bad … spending sharply snapped back. Last month (see here) we noted that the remarkable December spending contraction (-13.8% YoY) was likely to be followed by a spending binge in January, as in 2024. Nothing farther from the truth. Real spending in January roared back rising by 11.8%, with current expenditure rising by 7.4% YoY (-7.0% in December 2024), while capital expenditure rose by an eye-popping 97.1% YoY. Even though January spending likely reflects delays from the December close, the MoF appears to be frontloading fiscal spending again. Spending as a share of the annual budget reached 8.0%, the greatest over the last decade, and above the 6.8% 2016-2024 average. Spending will have to slow later in the year if the MoF plans on achieving its annual spending forecast of 2.7%.

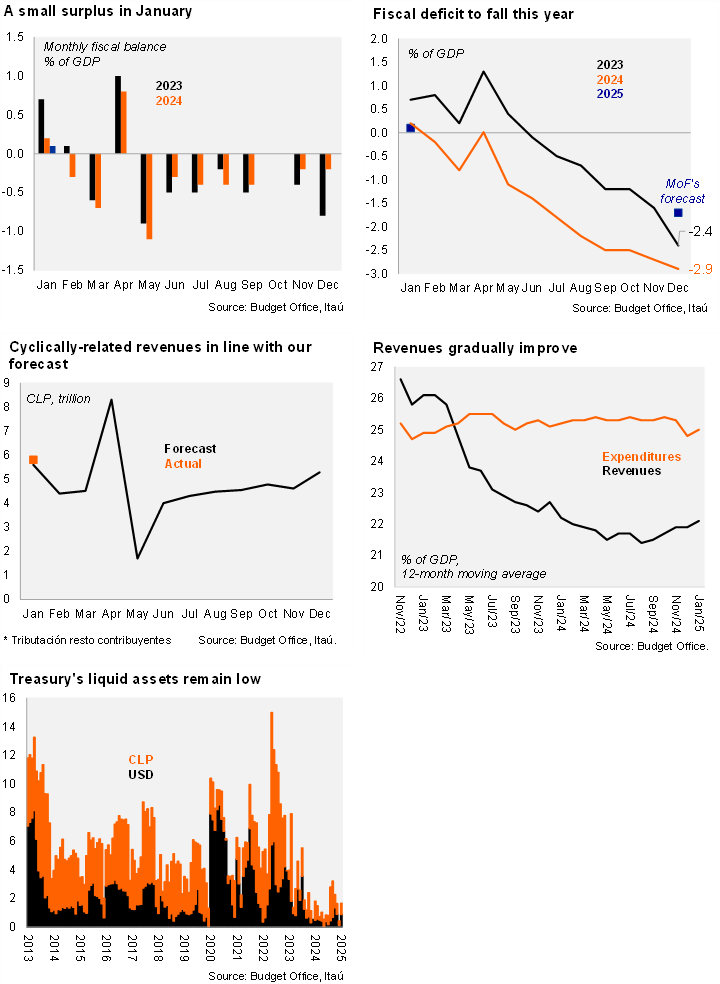

Even though revenues outperformed in the month, the spending bonanza led to a monthly fiscal surplus of only 0.1% of GDP, the smallest for the month in several years.

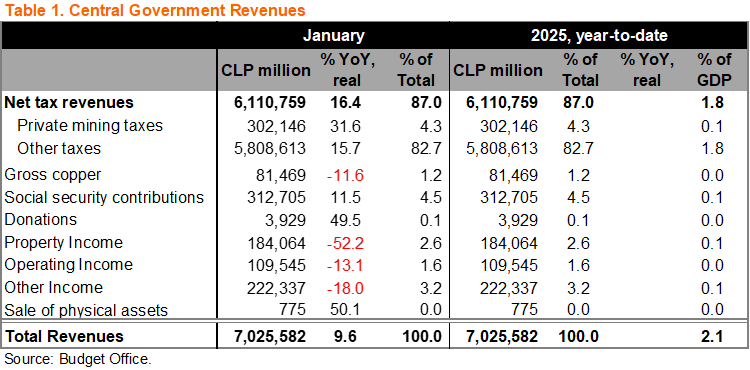

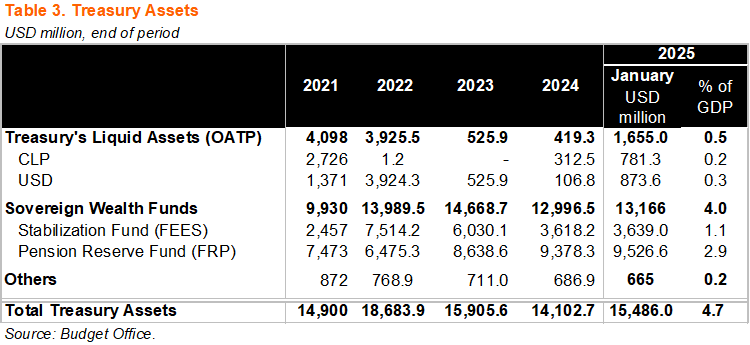

12-month rolling fiscal deficit remained unchanged at 2.9% of GDP in January. On a 12-month moving average basis as of the end of January, the central government’s revenues reached 22.1% of GDP, and expenditures 25.0% of GDP, leading to a cumulative deficit of 2.9% of GDP, unchanged from December 2024, down from 3.4% the previous month (deficit of 3.0% of GDP in January 2024).

Historically low liquid assets at the Treasury by the end of December. Liquid assets in the Treasury (Otros Activos del Tesoro Público) rose at the margin to USD1.65 billion (USD419 million by the end of December), the lowest January balance at least since 2011 (previous low was in 2024 with USD1.8 billion). AUM in the sovereign wealth funds were little changed, likely reflecting valuation effects. The Stabilization Fund (FEES) remained at USD3.6 billion, and the Pension Reserve Fund (FRP) was slightly up to USD9.5 billion.

MoF dollar sales to slow in March. Having sold a total of USD2.1 billion in the year through February, and without a weekly sales guidance yet for March, we believe the MoF could sell up to roughly USD400 million in March. This forecast is based on end-January dollar balances, USD sales in February, our projection for dollar-denominated revenues, and amortizations of dollar bonds. We envisage 2025 annual dollar sales at about USD8.4 billion (USD6.9 billion in 2024). Importantly, dollar sales finance the government’s fiscal needs (primarily in pesos), disregarding exchange rate considerations, consistent with Chile’s free-floating exchange rate regime.

Our take: The ugly … the stage is set for another structural deficit target miss in 2025. Following the large fiscal miss in 2024 (structural deficit of 3.2% of GDP, above the 1.9% target), spending dynamics at the start of 2025 suggest the MoF will follow a frontloaded strategy, as in 2024, on the expectation of a positive revenue surprise in April’s tax season. The MoF’s Public Finance Report already forecasts a structural deficit of 1.6% of GDP, above the 1.1% target, which would imply a large negative fiscal impulse of 1.8% of GDP. The most likely scenario is a revision to a somewhat watered-down structural deficit target for this year, and a spending cut of roughly 0.5% of GDP, which would contribute to meeting this year’s fiscal target. The Budget Office will release February’s fiscal data on March 30. Updated guidance on dollar sales for March should be announced soon.