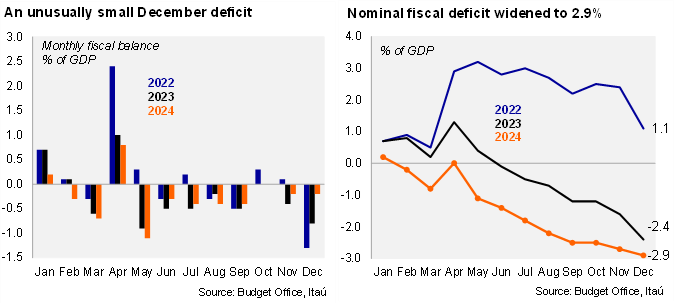

A smaller-than-expected fiscal miss in 2024, driven by an unprecedented expenditure contraction in December. According to the Budget Office’s preliminary data for December, the 2024 nominal fiscal deficit rose to 2.9% of GDP, from 2.4% in 2023, well above the official forecast (2.0%), close to our call (3.0%), and below other market forecasters. In our view, the slightly lower than-expected-deficit leads to a bittersweet end to a challenging year for Chile’s fiscal accounts. The 2024 nominal deficit was the greatest since the 7.7% of 2021, in the midst of the pandemic.

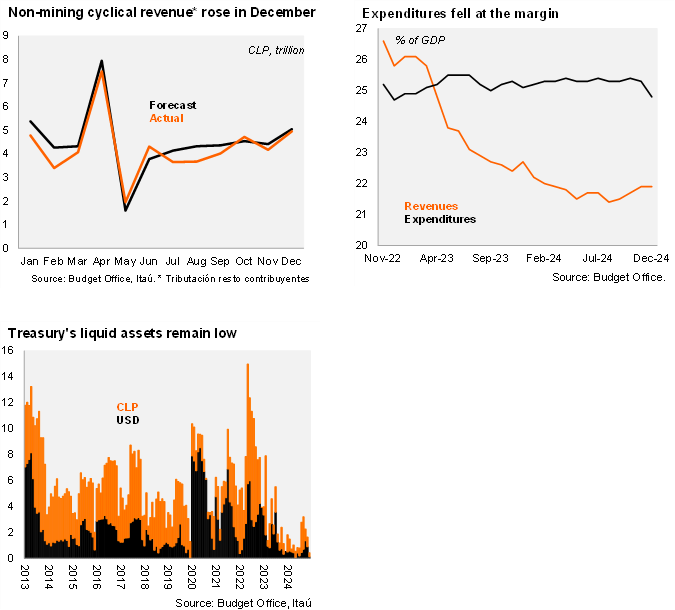

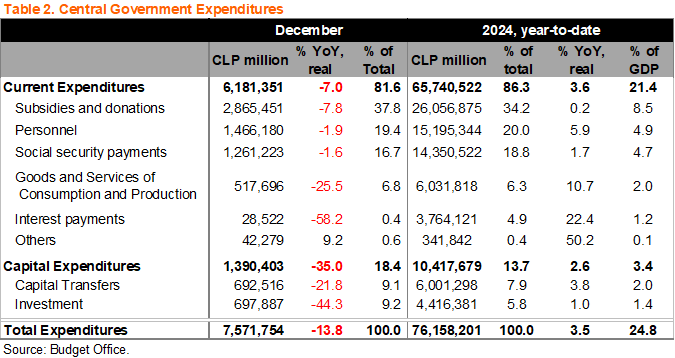

Revenue recovery continued but at a slower pace. As we’ve anticipated in previous months, the stalled real revenue recovery persisted in December, rising by 4.9% YoY (20.9% in November), mainly driven by cyclical factors and mining (also base effects due to the implementation of the revised royalty law, see Table 1); non-mining cyclically related revenues were essentially in line with our forecast (see chart), which may also reflect the effects of the tax compliance law (the local tax authority reported a ~0.3% of GDP in additional revenues towards yearend). The revenue recovery was in fact “too little, too late” as we had envisaged a few months ago (see here), with real revenues rising by 1.0% in 2024, improving from previous months, ending the year significantly below the MoF’s annual +5.3% forecast.

A remarkable spending contraction in December. Mimicking the spending contraction of December 2023, when real fiscal spending contracted by 5.6% YoY, real expenditures last December fell by 13.8% YoY, a double-digit annual decline not seen since the phasing out of the universal cash transfers that were implemented throughout most of 2021. Current expenditures contracted by 7.0% YoY, mainly driven by a decline in subsidies and donations, as well as spending in goods and services, which led to an annual execution of 101.5% of the budget. After an unusually strong first semester in capital spending, theses expenditures collapsed by 35.0% YoY in December, leading to an 86% execution of the annual budget. In the end, the unprecedented spending contraction in the month allowed for real expenditure growth in the year to converge to the MoF’s 3.5% forecast.

The nominal fiscal deficit rose to 2.9% of GDP in 2024, well above the MoF’s 2.0% deficit forecast (published in October) and last year’s deficit (2.4%). The unprecedented spending contraction in December and the ongoing improvement in revenues led to an unusually small deficit in December of 0.2% of GDP, significantly below the 2022-2023 average monthly fiscal deficit for the month of roughly 1.1% of GDP. As a result, the 2024 nominal fiscal balance fell to -2.9% of GDP, from -2.7% in November, and -2.4% in 2023.

12-month rolling fiscal deficit widened to 2.9% of GDP in 2024, from 2.4% in 2023. On a 12-month moving average basis as of the end of December, the central government’s revenues reached 21.9% of GDP, and expenditures 24.8% of GDP, leading to a cumulative deficit of 2.9% of GDP, down from 3.4% the previous month (deficit of 2.4% of GDP in December 2023).

Gross public debt creeping ever closer to the “prudent” level of 45% of GDP. Gross public debt reached an estimated 42.3% of GDP in 2024, above the 39.7% of 2023 and the 41.2% forecasted by the MoF in the Public Finance Report of February 2024. The miss mainly reflects the effects of the exchange rate depreciation; we estimate that a CLP100 depreciation leads to a 1.5% of additional gross public debt.

Debt financing off to a strong start early in the year. The Ministry of Finance announced their 2025 debt financing plan for a gross total of USD16 billion, in line with our forecasts, and consistent with the 2025 Budget Law’s limit. New financing accounts for roughly USD11 billion, and amortizations for USD5 billion. The MoF began implementing their plan with USD3.4 billion in foreign currency denominated bonds early in January and initiated local currency bond auctions in the end of the month, earlier than previous years likely due to the low cash balances and sizable foreign currency amortizations by the end of January. See our initial impressions of the 2025 financing plan here.

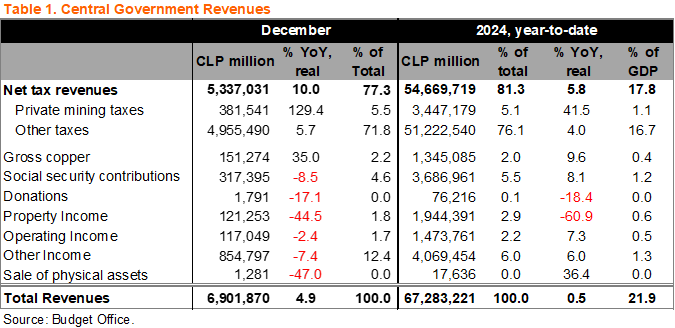

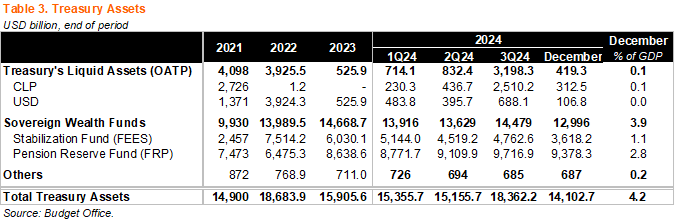

Historically low liquid assets at the Treasury by the end of December. Liquid assets in the Treasury (Otros Activos del Tesoro Público) fell again to USD419 million by the end of December (USD1.6 billion by the end of November), the lowest yearend balance on record (at least since 2007, previous low was in 2023 with USD526 million). AUM in the sovereign wealth funds were little changed in the month, likely reflecting valuation effects. The Stabilization Fund (FEES) reached USD3.6 billion, and the Pension Reserve Fund (FRP) USD9.4 billion. The Budget Office is expected to begin publishing AUM data this year on two funds which had not been publicly disclosed until now – the Plurianual Fund and Armed Forces Contingency Fund; both were approved by Congress along with the repeal of the Reserved Copper Law in 2019. We do not expect these funds to have accumulated significant funds since their inception.

Dollar sales to continue in February. Considering dollar inflows from the January foreign currency debt issuances (net of amortizations), projected mining-related revenue in the month, and January dollar sales for USD998 million, we believe the MoF will continue to sell dollars in February in line with their current guidance of up to USD300 million per week. A somewhat larger-than-expected issuance plan of foreign currency denominated bonds led us to revise our annual dollar sales forecast to roughly USD8.4 billion (see details of our initial forecast here). Importantly, dollar sales finance the government’s fiscal needs (primarily in pesos), disregarding exchange rate considerations, consistent with Chile’s free-floating exchange rate regime.

Our take: The MoF likely missed the 1.9% of GDP structural deficit target, as gross public debt continues to edge closer to the prudent debt limit of 45% of GDP. While the yearend balance was slightly better than our -3.0% of GDP forecast, spending is likely to bounce back materially in January, as was the case after the expenditure constraint of end-2023. The projected relief of the 0.2% of GDP spending adjustment for 2025 appears to be offset by discussions in Congress that would maintain a lower corporate income tax for small firms this year. Complying with the MoF’s projected fiscal consolidation path to a structural deficit of 1.1% of GDP relies on a significant additional spending adjustment and a solid revenue recovery. Following the 2024 fiscal miss and greater-than-expected erosion of the sovereign’s debt metrics, we expect the MoF to announce a spending cut in the near term. The MoF and Budget Office will publish the 4Q24 Public Finance Report with a preliminary close to 2024 and updated macro forecasts on Friday February 7. The Budget Office will release January’s fiscal data on March 3. Updated guidance on dollar sales for March should be announced during the first week of March.