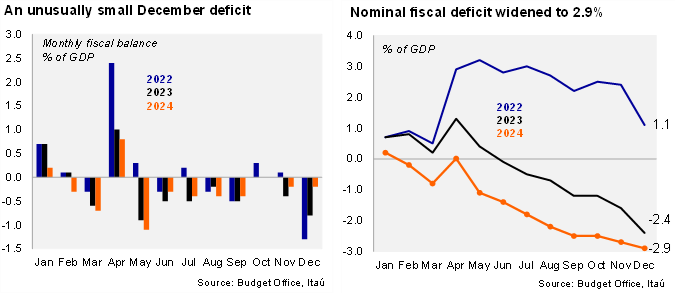

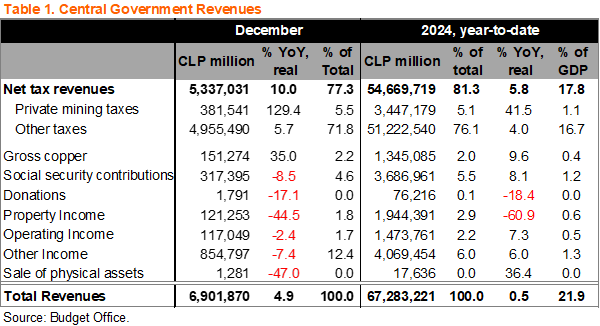

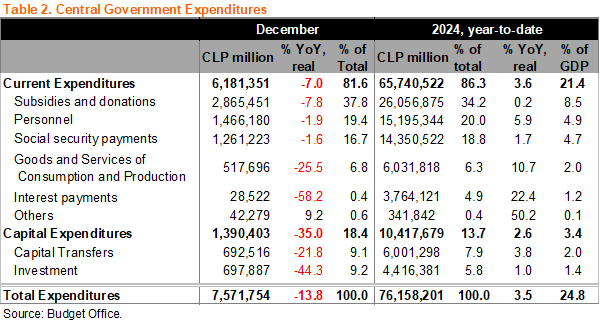

And that’s how the cookie crumbles… As we had anticipated in the aftermath of the April tax season (available here), the Budget Office’s 4Q24 Public Finance Report (available here) confirmed that the structural fiscal deficit in 2024 ballooned to 3.2% of GDP, well above the 1.9% official target, and 2.7% of 2023. The miss was primarily driven by weaker than expected revenues, as expenditures in the year were essentially in line with the MoF’s adjusted forecasts.

2025 nominal deficit revised higher, closer to our forecast. The 2025 nominal deficit forecast was revised up to 1.7% of GDP, up from 1% in the October forecast, and 0.3% in February 2024. We have maintained our 2025 1.8% nominal deficit forecast since November.

Another one bites the dust … the MoF already forecasts another miss for 2025. Even though the official 2025 structural fiscal deficit target reaches 1.1% of GDP, the MoF already forecasts a greater structural deficit of 1.6% of GDP (primary structural deficit of 0.5%). The fiscal impulse, as measured by the annual change in the primary structural balance would reach -1.4% of GDP.

Fiscal impulse projected to swing negative in 2025, if MoF forecasts prevail. The fiscal impulse, as measured by the annual change in the primary structural balance was positive in 2024 at 0.3% of GDP; that is, the primary structural deficit widened from 1.6% to 1.9%. The MoF’s 2025 forecast, with the above-target structural deficit of 1.6% of GDP, envisages a swift narrowing of the primary structural deficit to 0.6% of GDP, implying a very large negative fiscal impulse of 1.3% of GDP.

A challenging debt stabilization, now under even more stress due to the pension reform. The MoF’s forecasts consider that gross public debt peaked at 42.3% of GDP in 2024 (, would then fall to 42.1% by the end of this year, and then gradually edge down to 40.6% by 2029. In the near term, exchange rate dynamics and deficit financing are likely to lead even greater debt. Over time, risks of revenue underperformance and spending pressures pose risks to the stabilization of public debt. Data presented by the Autonomous Fiscal Council states that the recently approved pension reform (see here) has a gross fiscal impact of 1.2% of GDP per year by 2035 (peak), to be financed by an uncertain stream of permanent revenues of 1.5% of GDP sourced from the tax compliance law approved last year; risks tilt towards fiscal costs being greater and revenues lower.

Our take. Even though presidential and legislative elections will be held this year (November 16), we expect the MoF to announce an additional spending adjustment of at least 0.5% of GDP, and potentially a revision to a larger and less ambitious 2025 deficit target. In our view, the persistent misses of the fiscal target in recent years suggests Chile should target a structural surplus sooner than later, implying a material fiscal adjustment on the spending side is required. A much-needed replenishment of the Stabilization Fund (USD3.6 billion, 1.1% of GDP) to levels recommended by the IMF (5-7% of GDP) does not seem to be considered through 2029. January’s fiscal data will be published on March 3, and the 1Q25 Public Finance Report with the final 2024 data is scheduled for April 28.