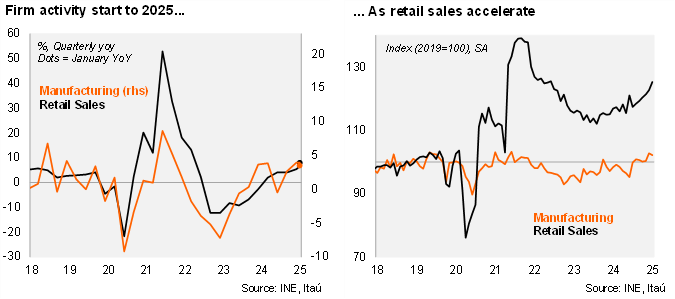

Retail sales and manufacturing surprised to the upside in January, while mining unwound part of the December boost. After a double-digit (11.7%) annual increase in mining in December, production fell by close to 7% MoM/SA at the start of 2025 leading to a 0.6% YoY increase. Manufacturing fell sequentially but still posted an above consensus annual increase of 3.5% (Itaú: 2%; Bloomberg: 2.4%). Food processing was key to the upside pull (+2.7pp contribution). Despite a soft real wage bill, retail sales remained upbeat, growing 8% YoY (5.8% in December), above market expectations (Itaú and Bloomberg consensus: 4.2%), sustaining a clear upward trend that is being boosted by the continued surge in consumer-tourism.

Retail sales momentum continued to accelerate. Total retail sales increased by 6.6% YoY during the January quarter (5.4% in 4Q), with durable retail sales rising 8.2% YoY and non-durable goods increasing 6.2%. Separately, total industrial production rose 3.9% in the quarter (4.4% in 4Q). Manufacturing growth came in at 4%, while mining rose an elevated 5%. In seasonally adjusted terms, retail sales increased 13.2% QoQ/saar (10.9% in 4; 0.6% in 3Q24), while manufacturing rose 5% QoQ/saar.

Our Take: We expect IMACEC in January to grow 2.7% YoY (6.6% in December), with risks tilted to the upside. Improving activity dynamics, amid still high inflation pressures consolidate our call that the central bank will hold rates at 5% this year. With imports of capital goods continuing to recover and consumer tourism persisting, our GDP growth call of 2.3% for this year has an upside bias. Nevertheless, borrowing costs above pre-covid levels, and elevated inflation may limit a faster recovery.