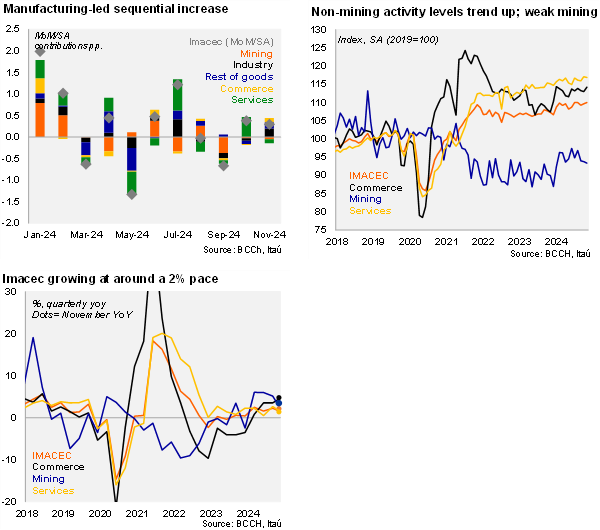

According to the Central Bank, the Monthly Index of Economic Activity (IMACEC) increased 0.3% MoM/SA, building on the 0.4% gain in October. The annual print came in at 2.1% (2.3% YoY in October). The activity performance was a notch above our 1.5% call and the Bloomberg median (1.7%). Even though mining fell sequentially, but still grew at a 3.5% annual pace. At the margin, activity dynamics were boosted by goods, particularly manufacturing (+0.2pp contribution). Commerce grew 1.1% MoM/SA and 4.8% YoY, likely supported by the significant rise in foreign tourism to Chile (particularly from Argentina). Softer business operations led to services ticking down 0.2% from November, leading to an 1.4% annual increase. Overall, non-mining activity increased a 2% YoY (2.3% in October). If activity levels are flat in December, the economy will expand by roughly 2.3% YoY in 2024 (Itaú: 2.2%; 0.6% in 2023). The carryover for 2025 would be 0.5%.

While the economy has posted two consecutive monthly increases, growth in the rolling quarter was a weak 0.2% qoq/saar, given the sharp monthly drop in September (mainly due to mining). If activity levels remain flat in December, annualized quarterly activity momentum would tick up to 0.5%. Non-mining GDP increased at a higher 1-9% QoQ/SAAR (3.8% in 3Q).

The outlook remains challenging. While business confidence (IMCE) and consumer confidence (IPEC) have improved throughout the year, both remain in pessimistic territory, and bank credit dynamics continue to contract over twelve months in real terms, suggesting that the recovery of non-mining investment will continue to lag. On the private consumption side, slack in the labor market, supply pressured inflation and elevated interest rates would prevent greater dynamism. However, tourism to Chile, mainly from Argentina, should continue to grow in the coming quarters, supporting trade, restaurants, hotels, among others.

Our Take: We expect the Chilean economy to grow 1.9% this year, near its potential. The central bank has a 1.5-2.5% forecast range for 2025. Recent downside surprises in the unemployment rate and activity growing around potential, amid weakening CLP dynamics and global uncertainty favor a strategy of inter-meeting rate cuts by the BCCh in its bid to continue to gradually lower the policy rate towards neutral (3.5%-4.5%). We expect a pause in the cutting cycle later this month, together with a guidance that highlights a cautious strategy ahead. The BCCh will publish the December IMACEC on February 3.