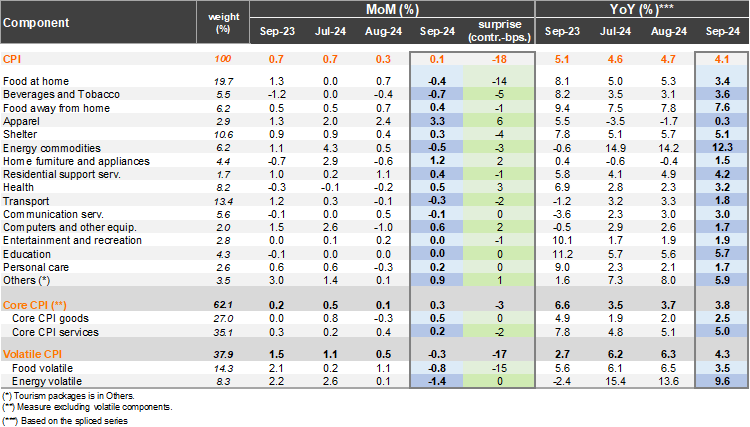

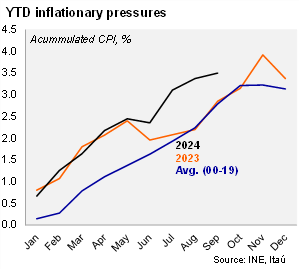

Consumer prices increased 0.09% from August to September, well below the central bank’s analyst survey (0.4%), the Bloomberg market consensus (0.3%), market pricing (0.27%), and our call of 0.26%. The most notable increases were in clothing and footwear, household equipment and maintenance, while food and non-alcoholic beverages contracted. With the monthly increase, annual inflation in the reference series reached 4.0% YoY (from 4.6% in August). CPI excluding volatiles rose by 0.3% MoM (0.2% in September last year; 0.1% MoM in August), with core goods rebounding (0.5% MoM) and core services more contained (0.2%). On an annual basis, core CPI reached 3.8% (reference series) from 3.7% in the previous month. Volatiles fell by 0.3% MoM, dragged by energy prices (-1.4%) and foods (-0.8%). The downside surprise to our headline CPI forecast was concentrated in the decline in food prices, despite the national independence holidays. Meanwhile, domestic transportation-related prices expectedly rose (interurban bus travel: +16.4% mom). While the downside surprise was led by volatiles, core price dynamics are only gradually edging up, insufficient to detract from the view that the central bank will continue to cut rates ahead.

Headline sequential pressures dip. Tradable prices were flat from August, leading the annual tradable variation to fall by 80bps to 3.5% YoY. Prior to geopolitical developments in October, global oil prices had underwhelmed, and the CLP was narrowing the gap with levels from last year, easing the pressures on tradable prices. Food prices fell 0.5% MoM, unwinding the gain in August and leading to an accumulation of 2.4% this year. Separately, energy prices contracted 1.4% MoM (with gasoline prices falling 1.7% and no electricity adjustment). Nevertheless, energy prices have accumulated a 6.8% rise so far in 2024, leading price pressures. Since April, accumulated condominium fees have not shown a significant increase, a risk that lies ahead given the several past and upcoming electricity price adjustments. Non-tradables increased 0.3% MoM, and 4.7% YoY (reference series; -0.2pp from August). At the margin, we estimate that inflation accumulated in the quarter was down to 2.9% (SA, annualized), from 4.5% in 2Q24. Meanwhile, core inflation rose to 4.5% (SA, annualized, 3.3% in 2Q24; 3.3% average during 2011-19), lifted by core services.

Our Take: Anchored inflation expectations, and the lagged effect of a still-contractionary monetary policy will support the disinflation process. We see inflation of 4.5% this year, as upside electricity risks and past CLP depreciation pressures are offset by widespread retail sales events. We expect inflation to fall to 3.3% next year. Nevertheless, geopolitical developments in the Middle East that keep global oil prices elevated, disrupt supply-chains and pressure the CLP, pose risks towards a slower disinflation process. For October, we preliminarily expect a 0.6-0.7% increase with a rebound in volatile prices and a large electricity price adjustment (15%). Yet, the effect of retail sales events at the start of the month and the possibility that the implementation of higher energy prices is delayed to November pose downside risks to the call.