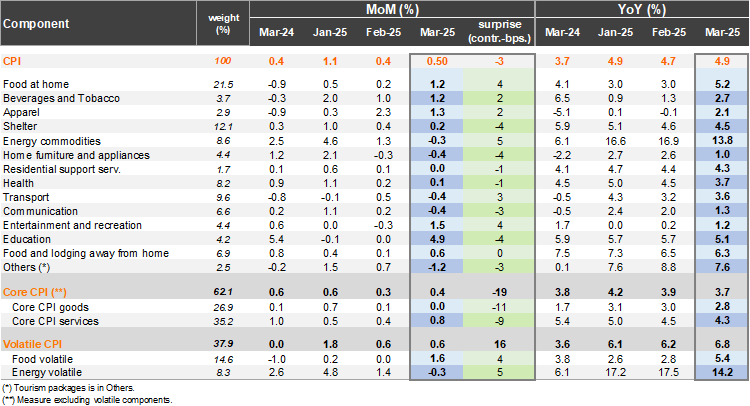

The headline CPI increase of 0.51% from February to March was in line with our call, as well as the Bloomberg market consensus, the market curve and the implicit estimate from the 1Q IPoM. The price pull was led by food prices (1.2% MoM; +27bp contribution) and the 4.9% MoM educational price adjustment ( +21bps). The transport division countered the upside pressures, falling 0.8% MoM (-11bps), following drops in interurban bus fares and gasoline prices. Core prices (excluding volatile items) increased 0.4% from February, a significant downside surprise to our 0.75% call (0.8% implicit in the 1Q IPoM). The downside core surprise stemmed from a lower education price hike, rental fees, and domestic services. On the goods side, new vehicles and computers played a role. Overall, second round effects from the prior electricity adjustments remain contained.

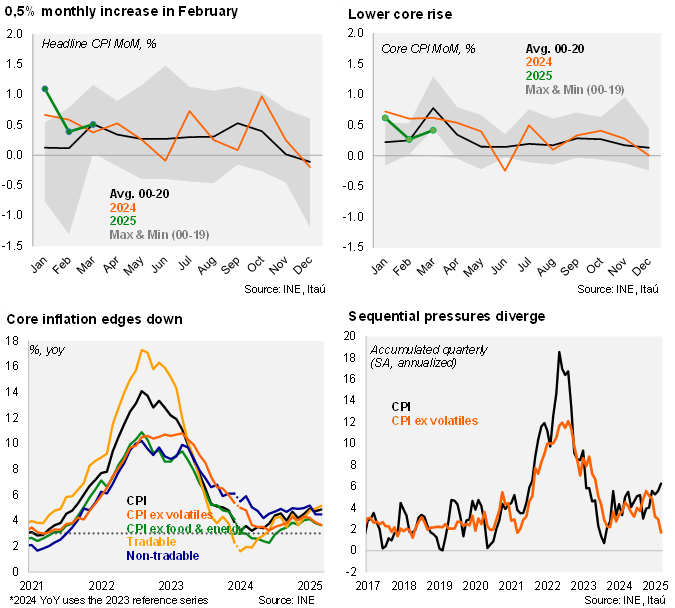

Core inflation is evolving favorably. In annual terms, headline inflation ticked up 20bps to 4.9%. Annual inflation has been above the 3% target since early 2021. Inflation averaged 4.8% during 1Q25, similar to the 4.9% estimate in the 1Q IPoM. Core inflation ticked down 20bps to 3.7%, the lowest rate since August last year. Core goods inflation dropped 0.2% MoM and 2.8% YoY%, while core services dipped 20bps to 4.3%. Core inflation averaged 3.9% during the quarter, 10bps below the IPoM scenario. Volatiles rose 0.6% MoM, boosted by food items, and resulting in an annual increase of 6.8% (+60bps). Sequentially, the annualized headline inflation accumulated over the last quarter reached 6.3%, while core pressures came in at a low 1.7%, down from a recent 5.6% peak in the October ’24 quarter.

Our Take: Core inflation dynamics appear well-behaved. We expect consumer prices to rise between 0.1% and 0.3% in April (4.5% YoY). During the second half of the year, a milder electricity price adjustment is likely to materialize (+10bps), the first since January-25. We foresee a YE rate of 4.1%, with core inflation closer to 3.5%. Nevertheless, the effects of lower oil prices, potential trade diversion of ex-US manufactured goods to Chile, and a dent to domestic demand may lead to an even swifter disinflation process, outweighing the effects of the recent depreciation of the exchange rate in the context of low margins for firms. If inflationary pressures and expectations consolidate the downward bias, the central bank will likely implement rate cuts ahead of our 1H26 scenario (to 4.5%).