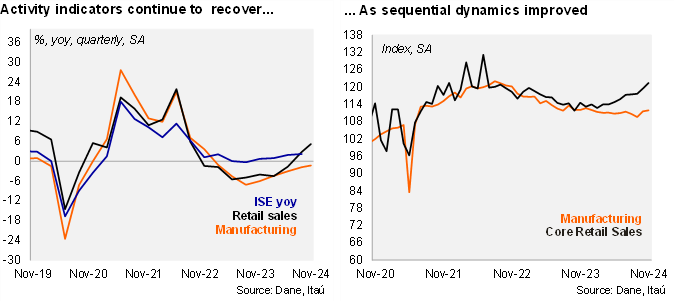

Retail sales surprised strongly to the upside while manufacturing returned to negative territory in November. In annual terms, retail sales increased 10.4% yoy in November (+9.8% in the previous month), well above the Bloomberg market consensus and our forecast both at 4.6%. Core retail sales (excluding fuels and vehicles), increased 1.6% from October (mom/sa), leading to a 7.0% yoy increase, (1.5% mom/sa and 5.9% yoy in October). Meanwhile, manufacturing increased by 0.3% mom/SA, leading to a -0.8% yoy contraction (1.1% yoy and 1.8% mom/sa in October), lower than the Bloomberg market consensus of -0.6% but better than our -1.4% call. We now estimate the monthly activity indicator (ISE) to increase 2.2% yoy, to be published on Tuesday 21, mainly driven by agriculture, commerce and services sectors.

Manufacturing levels improved at the margin. Manufacturing was boosted by sugar production, transport equipment and beverage production. During the quarter ending November, manufacturing fell 1.3% after falling 1.8% in 3Q24. At the margin, manufacturing dropped 0.1% qoq/saar (-1.2% in 3Q24). Manufacturing levels are now 8.4% above pre-pandemic levels (18% peak during 3Q22).

Retail sales were boosted by durable goods and vehicle and communication equipment. During the quarter ending in November retail sales increased 7.0% yoy (+2.8% in 3Q24), while core retail sales rose by 5.2% (+2.8% in 3Q24). At the margin, core retail sales increased 9.5% qoq/saar. Core retail sales now are 17.3% above pre-pandemic levels (+27% by mid-2022).

Our take: The evolvement of activity indicators confirm the trend of a gradual activity recovery observed in 3Q24. Nevertheless, activity performance has been in line with the Central Bank's expectations, so we do not discard BANREP pausing the easing cycle at the first monetary policy meeting of the year, as both analysts' and market inflation expectations continue to diverge from the target.