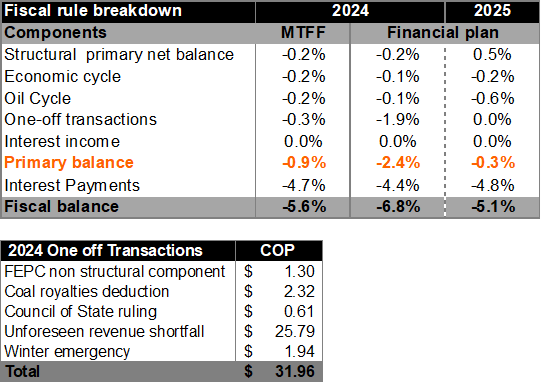

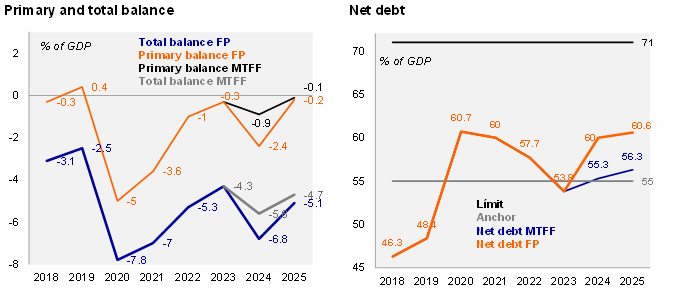

Lower-than-expected tax revenue in 2024 hampered the government's ability to achieve the initial deficit target of 5.6% of GDP (4.3% of GDP in 2023). The MoF's updated fiscal plan showed an eventual 6.8% fiscal deficit (the largest since 2021, 7.0% of GDP) due to a revenue shortfall of 0.9% of GDP that exceeded the expenditure cut of COP28.4 trillion (1.7% of GDP). More importantly, the primary balance deteriorated significantly, rising from -0.3% of GDP in 2023 to -2.4% of GDP in 2024, driven by one-offs amounting to 1.9% of GDP (COP31.9 trillion). Within these one-offs approved by the Superior Council of Fiscal Policy (CONFIS), the MoF included a non-anticipated revenue shortfall of COP25 trillion (1.5% of GDP), with the remainder explained by the Council of State’s decision over the deductibility of coal royalties from income rent. Overall, public debt rebounded substantially from 53.8% of GDP to 60% of GDP in 2024. Despite the Fiscal Council’s warnings and the overall outcome of fiscal accounts, the government claims to be in compliance with the fiscal rule.

In 2025, regaining fiscal credibility is at stake, but revenue estimates may once again be too upbeat. For 2025, the MoF projects growth of 2.6%, in line with the central bank's estimate (Itaú: 2.2%), which increases fiscal challenges given the optimistic revenue projections for the second year in a row. The government expects tax revenues to increase by 22.6% YoY to COP 300 trillion, a figure that not only implies an additional COP 55.2 trillion in revenues compared to the 2024 outcome (3.1% of GDP). In this context, the fiscal deficit target for 2025 remained stable at 5.1% of GDP, implying a strong fiscal adjustment with a primary balance of -0.2% of GDP. Debt is expected to increase slightly from 60.0% of GDP in 2024 to 60.6% of GDP, moving further from the debt anchor (55% of GDP).

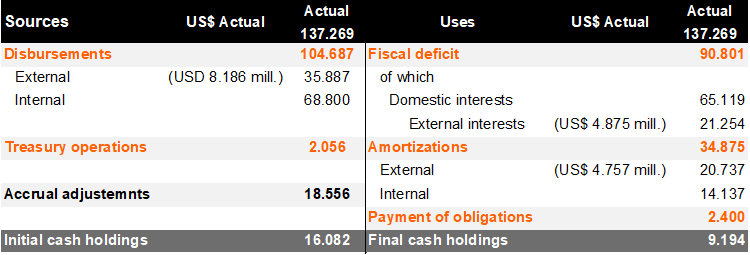

External debt servicing to reach a record high in 2025. The central government’s gross financing needs in 2025 are estimated at COP 121 trillion (excl. the primary deficit), COP 10.4 trillion lower than the previous estimate published in the MTFF. Interest payments amount to COP 86.3 trillion (71% of total financing excl. primary deficit; 76.4% in 2024) and amortization to COP 34.9 trillion. Although internal amortization has decreased significantly (COP 12.7 trillion) compared to the MTFF estimates due to the debt swap strategy implemented by the MoF, this account shows an annual increase of 45.5%. In fact, 2025 is set to be a record year for external debt obligations, with external payments of USD 9,632 million (compared to USD 7,946 million in 2024).

The targeted financing strategy is 66% in local currency and 34% in foreign currency ( 61% / 38% indicated in the MTFF). Specifically, the government plans to finance a deficit of COP90 trillion (vs COP155 trillion in 2024) with domestic financing set at COP68.8 trillion (vs 65.9 trillion in 2024). Debt auctions in 2025 remain stable compared to the MTFF at COP 45 trillion (vs. COP 40 trillion in 2024), green bond issuance remains at COP 1.5 trillion, and funding from public entities is estimated at COP 22.3 trillion (vs. COP 22.7 trillion in 2024). On the external side, the MoF plans to raise USD 8,186 million (1.8% of GDP), USD800 million less than the amount unveil in June after the pre-funding operations from the global bond issued in 4Q24. According to the exiting public credit director, the 56% of external financing is expected through multilateral loans (USD 4559 million), while the remainder of USD 3,600 million is to be risen through global bonds issuance in international capital markets.

Our take: While the 2024 fiscal deficit is in line with the Fiscal Council's warnings, the 5.1% fiscal deficit forecast for 2025 seems difficult to achieve without an expenditure cut of at least COP 40 trillion (2.4% of GDP) and the adoption of a new tax bill, amid high revenue estimates. In the absence of structural measures on both the revenue and expenditure side, the primary deficit target of -0.2% of GDP could easily widen to -1.7% of GDP. In addition, the assumption of interest payments of 4.8% of GDP appears conservative and the fiscal imbalance in 2025 could move towards 6.5% of GDP. The above challenges to the fiscal consolidation process are in line with S&P's recent affirmation of the negative outlook on the 'BB+' rating. Currently, Colombia is rated non-investment grade by S&P and Fitch, while Moody's maintains Colombia's investment grade rating at Baa2 (outlook stable).