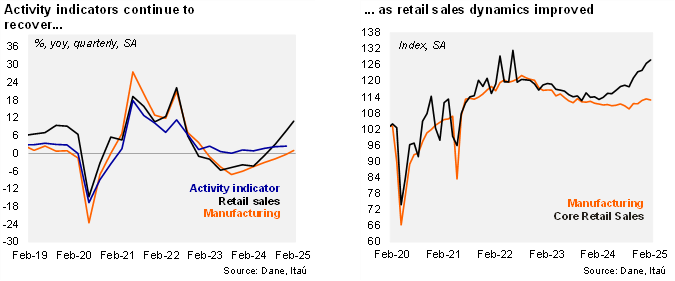

While retail sales remained upbeat, manufacturing surprised to the downside in February. In annual terms, retail sales increased 7.5% yoy in February (+10.2% in the previous month), in line with the Bloomberg market consensus of 7.5%, but below our +12.5% call. Core retail sales (excluding fuels and vehicles), increased 1.0% from January (mom/sa), leading to a 7.8% yoy increase (+10.7% yoy in December). Retail sales were boosted by computer equipment and vehicles, but partially countered by fuels. Meanwhile, manufacturing fell by 0.3% mom, leading to a 1.2% yoy contraction (+1.8% in January), well below the Bloomberg market consensus of +1.7%, and our +3.6% call. Manufacturing was dragged by fuels, beverages and mineral production.

Activity momentum remained strong at the margin. During the quarter ending in February, manufacturing increased 0.9% yoy (+0.7% in 4Q24). At the margin, manufacturing increased 7.8% qoq/saar, above the 5.0% in 4Q24 and -1.4% in 3Q24. During the quarter ending in February, retail sales increased 8.5% (+9.0% in 4Q24), while core retail sales rose by 8.3% (+7.1% in 4Q24). Sequentially, core retail sales increased 18.8% qoq/saar (from +17.2% in 4Q24 and +8.3% in 3Q24).

Our take: Activity continues to gradually recover, driven by domestic demand. Heightened global policy uncertainty and lower oil prices may limit the recovery, mainly affecting manufacturing production. We expect the economy to grow 2.3% this year, but with a downside bias (above from the 1.7% in 2024).