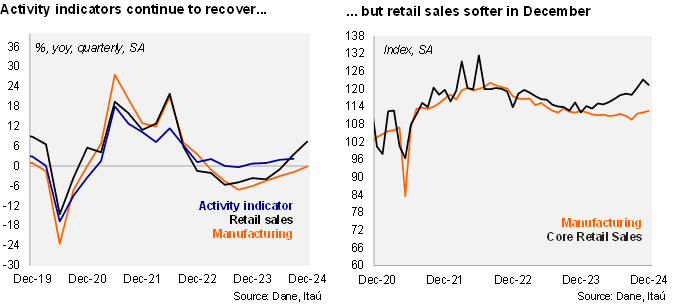

Activity closed 2024 with mixed signals, with manufacturing increasing sequentially, but retail sales corrected down. Retail sales increased 7.8% yoy in December (10.3% in November), below the Bloomberg market consensus of +8.8% and our +8.5% call. Core retail sales (excluding fuels and vehicles) fell 1.5% from November (MoM/SA; +2.3% registered in the previous month), leading to a +6.6% yoy rise (+8.4% previously). Meanwhile, manufacturing increased by 0.5% mom (+0.4% in November), leading to a 1.9% yoy rise (-0.6% previously), above than the Bloomberg market consensus of +0.6% and our -0.4% call. Overall, we expect GDP growth of 2.2% in the final quarter of 2024 (to be released on February 17), leading to a growth close to 1.8% of GDP during 2024 (0.6% in 2023).

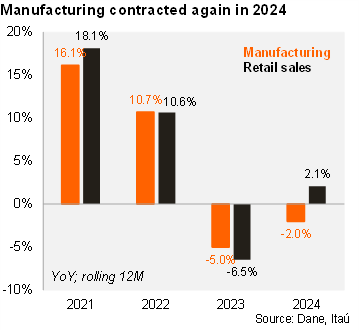

Manufacturing levels remained low in 4Q24. During the final quarter of the year, manufacturing increased 0.8% yoy (1.4% drop in the 3Q24). At the margin, manufacturing increased 5.3% qoq/saar (-1.4% fall in 3Q24). Manufacturing levels are now 9.1% above pre-pandemic levels (down from a near 18% peak during 3Q22). For the full year, manufacturing contracted 2.0% yoy (-5.0% in 2023).

Retail sales momentum in 4Q improved. In 4Q24, retail sales increased 8.9% (2.8% rise in 3Q24), while core retail sales increased 7.0% (+1.7% in 3Q24). At the margin, core retail sales rose by 12.7% qoq/saar, (+8.7% in 3Q24). Core retail sales now sit just 16.9% above pre-pandemic levels (+24% by mid-2022). Overall, retail sales increased 2.1% last year, partially offsetting the 6.5% drop in 2023.

Our take: The activity data signals domestic demand that continues to recover. We expect the economy to grow 1.8% last year (above from the 0.6% in 2023) and to grow above 2% in 2025 amid lower average interest and inflation rates.