Retail sales increased sequentially, while manufacturing fell at the margin in August. In annual terms, retail sales increased 5.2% in August, well above the Bloomberg market consensus of +2.3% and our +1.7% call. Core retail sales (excluding fuels and vehicles) increased 0.6% from July (MoM/SA), leading to a 5.2% YoY increase (-1.1% in July). Meanwhile, manufacturing fell by 0.6% MoM/SA, leading to a 1.8% YoY contraction (+2.0% previously), slightly below the Bloomberg market consensus of -1.4% and our call of -1.5% call. The data puts an upside bias to our estimate for the monthly activity indicator (1.3% YoY expansion, to be published on Friday 18).

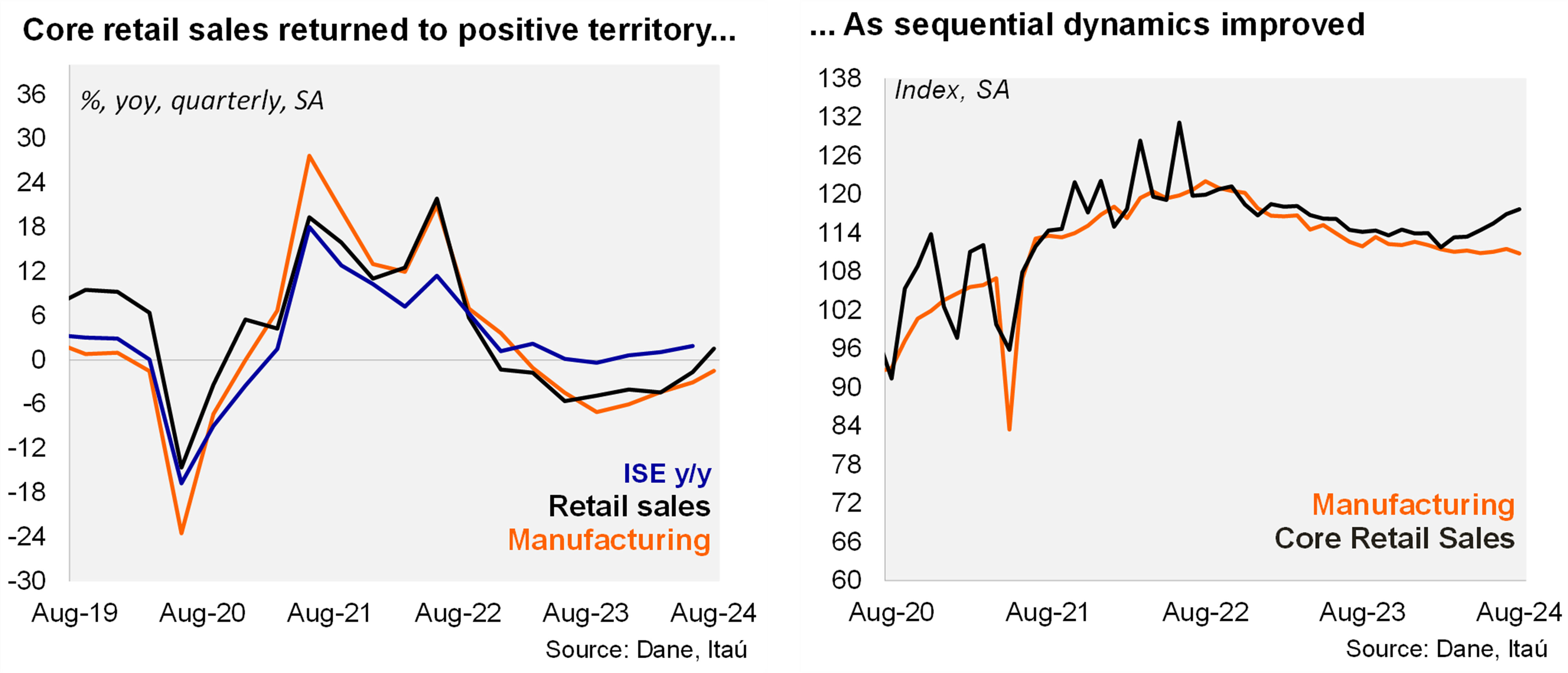

Manufacturing levels remained weak. Manufacturing was dragged by vehicle spare parts as well as clothing and textiles. During the quarter ending in August, manufacturing fell 1.6% (in line with the fall in 2Q24). At the margin, manufacturing contracted 6.4% qoq/saar, similar to 2Q24. Manufacturing levels are now 7.4% above pre-pandemic levels, falling from a near 18% peak during 3Q22.

The retail sales increase was boosted by communication equipment, vehicles and motorcycles. During the quarter ending August, retail sales increased by 2.8% YoY (0.6% drop in 2Q24), while core retail sales rose by 1.7% (-1.3% in 2Q24). At the margin, core retail sales improved to 10.8% qoq/saar (+5.2% increase in 2Q24). Core retail sales now sit 14% above pre-pandemic levels (+27% by mid-2022).

Our take: We expect the economy to grow 1.8% this year (0.6% in 2023), and 2.4% next year. Activity is advancing in line with the central bank's scenario, while inflation continues to fall and global financial conditions ease. We expect BanRep to accelerate the pace of the cycle with a 75bp cut later this month, but another 50bp cut cannot be ruled out.

Vittorio Peretti

Carolina Monzón

Juan Robayo

Angela Gonzalez