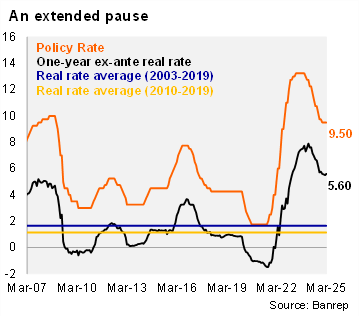

In yet another divided decision, BanRep kept the policy rate at 9.5% for a second consecutive meeting. The decision was in line with the Bloomberg market consensus, but above our call for a 25bp cut. The decision was split, with four members voting to pause, while three members supported a large 50bp cut. The meeting included votes from three new members (Avila, Moisa, Giraldo), who we also believe favored a cut. Governor Villar highlighted the increase in the February CPI, and still present inflationary risks due to fiscal uncertainty as justifications to stay on hold. Following the decision, the one-year ex-ante real sits at 5.6% (using the monthly analyst survey; +5bps from the previous meeting in January), well above BanRep’s neutral rate estimate of 2.7% in 2025.

The technical staff revised growth estimates higher. GDP growth is now seen at 2.8% (+0.2pp revision), with both the coincident indicator for January and other high-frequency data reflecting a domestic demand recovery.

Disinflationary process will continue, but upside risks remain. Governor Villar remarked that the technical staff’s CPI projection for the end of this year remained at an elevated 4.1%, a key factor behind holding rates. Governor Villar believes inflation dynamics will be more favorable in upcoming months, opening the door to resuming the rate cutting path.

The MoF has not ruled out a new financing law. Governor Villar noted that fiscal uncertainty can lead to greater country risk premium, raising long-term financing rates and affecting monetary policy. New finance minister, Avila, highlighted in-line with estimated revenue intake during 1Q25, and ruled out spending cuts that would compromise the government's national development plan.

The global scenario brings a wave of uncertainty. Discussions of higher tariffs may generate pressure on prices, while uncertainty in international markets could heighten currency volatility.

Our take: Once again the decision was a coin toss. Fiscal risks loom large, weighing on the majority of the Board. We expect the gradual disinflationary process to resume in March, however, there are still upside services and regulated price risks. We will likely revise our 8.0% yearend 2025 rate call higher. The next meeting is on April 30. The minutes of the meeting will be released on Thursday.