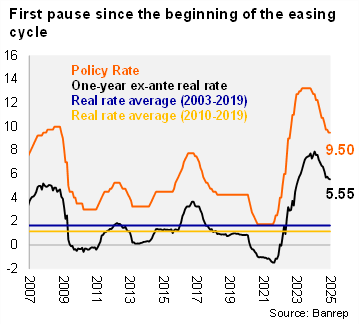

Adopting a more cautious stance following significant market volatility, BanRep decided to keep the interest rate unchanged at 9.5%. The Bloomberg market consensus and our call pointed to a 25bp cut. This is the second consecutive hawkish surprise and the first pause in a 375bp cycle that started in December 2023. The decision was split, with five members voting to keep the rate stable, one favored a 25bp cut, and the other a 50bp reduction. At the December meeting, the two dissenting voices had favored even larger cuts. Governor Villar highlighted headwinds to the disinflation process following the PPI increase, a large real minimum wage increase, and a climb in inflation expectations. Following the decision, the one-year ex-ante real rate fell to 5.5% (using the monthly analyst survey; -5bps from the previous meeting in December), well above BanRep’s real neutral rate estimate of 2.6% in 2025. Finance minister Guevara – a voting member in BanRep’s board - indicated the government will continue to pursue a downward interest rate trajectory.

A more challenging disinflationary process. In December, President Petro decreed a nominal minimum wage hike of 9.5% yoy (+4.2% real yoy) and a transport subsidy hike of 11% nominal yoy (5.8% real yoy). The measures will sustain inflationary pressures. With BanRep maintaining the goal of reaching the inflation target range by the end of 2025, the decision to pause the cutting cycle is coherent with accumulating information to understand the effects of above-mentioned measures on the inflation path.

Technical staff revised growth expectations down. The technical staff estimates GDP growth of 1.8% in 2024 (1.9% previously expected) and 2.6% in 2025 (2.9% in the last IPoM) in an environment of fiscal and COP uncertainties.

Global financial conditions tightened. Governor Villar remarked that external financial conditions tend to become tighter in the face of a more protectionist policies, which may end up having domestic inflationary impacts amid a stronger global dollar. Villar also referred to an apparent increase in global real long-term interest rates and its impact on domestic monetary policy. The board did not discuss a new reserve accumulation program, but Villar pointed out that it is not ruled out either.

Our take: In our view, the January decision was a coin toss between a mild cut or pausing. Fallout from tensions with the US and the final meeting of two of the more hawkish Board members probably were enough reasons to secure an on-hold majority. We expect rate cuts to resume in March (-25bps) with the Board’s makeup better reflecting the government’s stance. We cannot rule out a 50bp cut. We see an above consensus year-end rate at 8%.