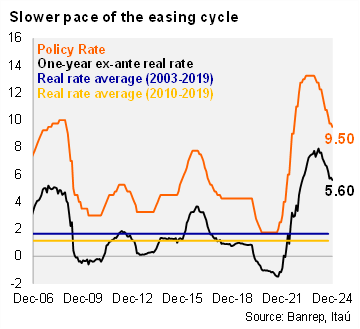

In a hawkish twist, BanRep cut the policy rate by 25pb, below market consensus and our call for a 50bp cut. The smaller cut is the first time the Board slows the pace of the easing cycle (50bp pace since March), reflecting concerns on global financial conditions and domestic fiscal uncertainty. The vote was split with five board members for a 25bp cut, one for 50bp and another for a 75bp cut. Following the decision, the one-year ex-ante real rate fell to 5.6% (using the monthly analyst survey; -9bps from the previous meeting in October), well above BanRep’s real neutral rate estimate of 2.4% in 2024 (2.6% in 2025). Governor Villar signaled that the technical staff expects that inflation will continue to converge, but more slowly than previously expected due to upward pressures on the exchange rate and their pass-through into prices. Exchange rate pressures are also due to tighter external financial conditions. Thus, Villar remarked that the expected monetary policy easing is lower than previously expected.

International and local risks led to a deceleration of the cycle. Governor Villar pointed out that the arrival of two new board members in February was not one of the reasons for the slowdown in the pace of cuts. The main reasons for the slowdown were risks related to international and local financial conditions, reflecting weaker sovereign risk levels and currency dynamics. Moreover, the press conference frequently referred to recent events in Brazil, reflect risks that should be considered in the BanRep Board's decisions. The materialization of these risks could pose financial stability risks and challenge the disinflation process.

A slower easing cycle path to ensure the inflation convergence. Governor Villar noted that the Central Bank’s goal is to achieve a convergence of inflation towards the target by the end of 2025 with a cautious stance. Going forward, the minimum wage increase remains a risk to inflation. The appropriate speed could be 50pb, 25pb or nothing accordingly. MoF Guevara highlighted a highly contractionary real interest rate. The new MoF Guevara remarked that the real interest rate continues to be highly contractionary, where its fall has been fundamental for the recovery of the economy, so there is room to increase its speed. However, Guevara acknowledges that the slowdown in the pace of cuts is due to fiscal uncertainty both locally and in the region. However, MoF Guevara gives a message of confidence in compliance with the fiscal rule this year.

Our take: The hawkish twist is likely to lead to repricing towards a higher terminal rate. Tighter global financial conditions along with sticky domestic services inflation, uncertainty over next year's minimum wage increase and short term stress in the fiscal accounts are likely to weigh on the next few decisions. Our 6.75% 2025 terminal rate call is likely to be revised up. The next meeting is on January 31.