Since the January meeting, the Board’s composition has changed with three new voting members, including two full-time board members and a new finance minister. We believe fundamentals favor a second consecutive pause, but the new composition of the Board swings the odds in favor of a 25bp cut to 9.25%. Overall, the decision is a coin toss with a 4-3 split expected regardless of the voting outcome. According to our study of Monetary policy cycles in Colombia, both easing and tightening cycles average four pauses per cycle (intermittent or prolonged pauses are not unprecedented).

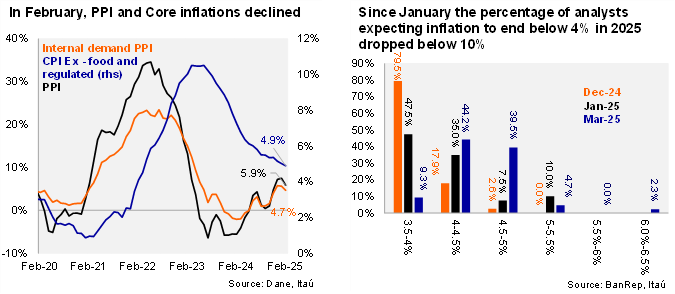

The balance of risks to inflation remains tilted to the upside, but some factors have receded. At the January on-hold decision, the majority expressed the need to assess the cumulative impact of several inflation shocks, such as the 9.5% nominal minimum wage hike, rising PPI pressure, and the weakened exchange rate. Since the first meeting of the year, services inflation has remained persistently high (7.2%) and year-end inflation expectations ticked up to 4.5% (BanRep: 4.1%) and the 2026 inflation expectation sits at 3.7% (BanRep: 3.1%). Breakeven inflation measures are also elevated. On the other hand, the PPI drop in February, easing core inflation and the notable COP recovery may alleviate prior concerns within the Board over inflation persistence.

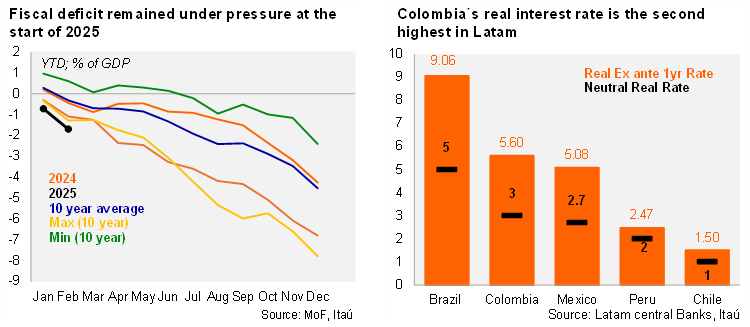

Fiscal policy is not helping. Fitch revised the outlook on Colombia’s BB+ rating to negative in early March. We estimate significant spending adjustments are required to meet this year’s fiscal target of 5.1% of GDP. The year has started off with a record high deficit through February. The deterioration in the fiscal situation may require an even higher real neutral rate going forward.

BanRep’s survey from around two weeks ago showed that 64% of analysts favored a 25bp cut in March, while 26% expected rates on hold. Similarly, the rate curve has priced a 9bp cut in recent weeks. Since January, President Petro named academics Cesar Giraldo and Laura Moisá to replace Jaime Jaramillo and Roberto Steiner (both on the hawkish side), and appointed German Avila as the fourth Finance Minister of the administration. These new members are perceived to lean more dovish and will likely push for a less contractionary policy stance to support the economic recovery.

Currently, Colombia's one-year ex-ante real rate stands at 5.60% (vs. 5.55% in January and 5.77% in December), the second highest in the region and well above BanRep's neutral estimate of 3%).

Our take: The musical chairs since the last meeting bring an elevated sense of uncertainty. The replacement of two hawkish members with two dovish names swings the odds in favor of resuming the cutting cycle with a 25bp move to 9.25%, despite our technical assessment that staying on hold has more weight. We expect a year-end rate of 8.0%, above the analyst consensus. The minutes of the meeting will be published on April 3.