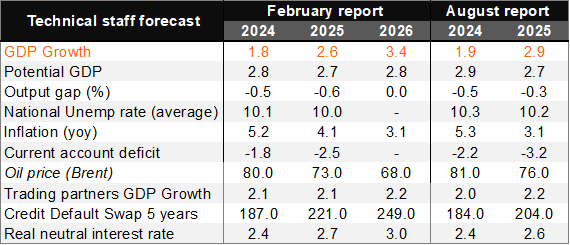

Banrep's technical staff revised inflation and the real neutral interest rate up. In its latest Monetary Policy Report, the year-end inflation forecast was revised up by 0.9pp to 4.05% (Itaú: 4.2%; 5.2% in 2024).The increase was driven by the significant real minimum wage adjustment (4.3pp) that in part is behind delaying the inflation convergence to the target to 4Q26 (from 4Q25 expected at previous IPOM). Regarding monetary policy, the central bank staff's baseline scenario implies a policy rate path that is, on average, above the analysts' expectations (which see the policy rate at 7.3% in 4Q25 and 6.25% at the end of the policy horizon). At the same time, the staff increased the estimated real neutral rate by +0.1 percentage point to 2.7% this year and by 0.3 percentage point to 3% in 2026, reflecting both a higher global real neutral rate and an upward trend in the risk premium. The activity outlook is more downbeat, with the 2024 forecast down 0.1pp to 1.8% (Itaú: 2.0%; 0.6% in 2023) and -0.3pp to 2.6% for this year.

The balance of risks for inflation remains tilted to the upside. The core inflation forecast for YE25 increased by 86 bps to 3.90%, just below the upper limit of the target range (2-4%). Core inflation in 2026 was also raised by 11bps to 3.14%. Pressures on services CPI are skewed to the upside due to the prevalence of strong indexation mechanisms, and the expected passthrough from labor costs to inflation. Regulated CPI was raised by 43 bps to 4.93% in 2025 and up to 3.2% in 2026. Nevertheless, this still implies strong disinflation from the 7.31% last year, on the expectation of easing gas supply constraints and milder energy prices adjustments.

A higher risk premium also adds pressure on inflation and on the neutral rate. Beyond services and strong indexation mechanisms, the staff acknowledged fiscal and external uncertainty weigh on the inflation convergence path through FX passthrough. BanRep's Technical staff see the Fed cutting twice in 2025, /four cuts seen previously). The implementation of global tariffs, and tighter global financial conditions narrows the room for local easing ahead. The real neutral rate is now seen at 3% in 2026, well above the historical average of 1.5%.

The negative output gap is expected to only close by 4Q26. According to staff estimates, the output gap closed 2024 at -0.5% of GDP and is expected to widen to -0.8% of GDP as of 3Q25 (-0.3% at the previous IPOM). As the balance of risks to growth remains tilted to the downside, a positive output gap is no longer expected at any point in 2026. Overall, excess capacity is expected to support the disinflation path towards the target by December 2026. Amid high uncertainty over potential growth, the estimate remained just below 3% for the forecast horizon.

A narrower current account deficit. The staff projects the CAD to narrow to 1.8% of GDP in 2024 (2.2% of GDP in the previous IPOM). The lower-than-expected CAD is driven by favorable dynamics in services, the income deficit and transfers. In 2025, the CAD is projected at 2.5% of GDP (3.2% of GDP in the previous IPOM).

Our take: BanRep’s hawkish decisions since December reflect caution amid rising inflation pressures. With prevalent indexation and fiscal uncertainty, a gradual cutting path is most likely. Nevertheless, the new Board’s composition could be inclined for larger cuts. We see a yearend rate of 8.0%, well above the analysts' consensus (7.0%). The minutes of January’s meeting will be released later today. Ahead of the March monetary policy meeting (31st), the Board will receive two CPI prints, and the CAD and GDP figures for 4Q24.