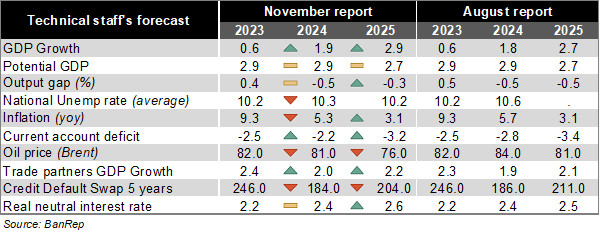

BanRep’s technical staff revised GDP up and short-term CPI down, while outlined an interest rate path that, on average, is above analysts’ expectations (9.0% yearend). Activity this year is now seen growing 1.9% (0.1pp above July’s scenario, 0.6% in 2023), and 2.9% for 2025 (2.7% in the previous report). The staff’s 2024 yearend inflation forecast was revised down by 0.4pp to 5.3% (Itaú: 5.6%; 9.3% last year), while YE25 CPI was lifted 5bps to 3.10% (Itaú: 3.6%). Regarding monetary policy, the central bank staff’s baseline scenario implies a policy rate path that, on average over the following eight quarters, is somewhat above the analyst’s expectations of 9.0% by yearend, and 6.0% by YE25 (implying that an acceleration from the 50bp cutting pace is not incorporated in the short-term). The estimated neutral rate was retained at 2.4% for this year (5.4% nominal) but revised up 10bps to 2.6%.

Service inflation pressures remain. The YE24 core inflation forecast ticked up 10bps to 5.1% due to higher-than-expected rent prices. For next year, the core inflation outlook is down 40bps to 3.0%. Services CPI pressures are skewed to the upside due to the prevalence of strong indexation mechanisms and the uncertainty around minimum wage adjustment in 2025. The downward revision in total inflation for this year was due to more favorable food and regulated price dynamics (electricity and fuel prices). The technical team highlights the exchange rate, supply shocks on food prices and adjustments in regulated prices as risks to monitor.

A smaller negative output gap expected. The 2024 output gap is still seen at -0.5%, but narrowed to -0.3% for next year (-0.5% in the previous report). Potential growth remained stable at 2.9% for this year and 2.7% for 2025. The upward revision in the GDP growth forecast for next year is driven by a stronger boost from domestic demand, coupled with less restrictive global financial conditions compared to the previous scenario.

A smaller current account deficit. The technical staff expects the CAD to narrow to 2.2% of GDP in 2024 (60bps below August’s call; 2.5% in 2022). A lower-than-expected CAD is due to favorable services, income deficit and transfer dynamics. For next year, the CAD is seen at 3.2% (20bps narrower than in the previous report). Moreover, the technical staff foresees a less restrictive global financial conditions compared to the previous scenario, with a more dovish outlook for the Fed's interest rate cut path, coupled with a slight fall in local risk premium.

Our Take: Domestic fiscal noise stemming from the regional distribution reform, along with increased global financial volatility mean the bar to accelerate the pace of the rate cutting cycle in the near-term is high. The minutes of October’s meeting will be released later today (50bp cut to 9.75%). The final policy meeting of the year will take place on December 20.