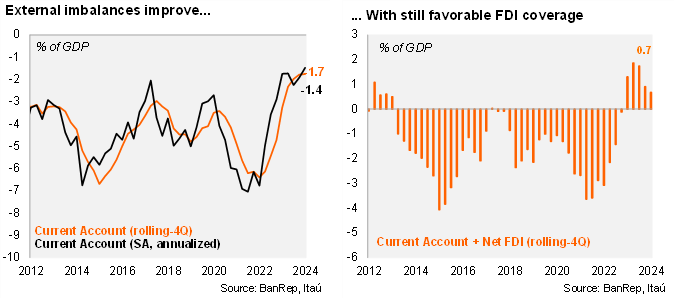

The CAD once more came in below expectations. A USD 1.7 billion current account deficit was registered in the third quarter of the year (remaining broadly stable from 3Q23), equivalent to 1.6% of GDP. The deficit was far smaller than the Bloomberg market consensus and our call of USD 2.4 billion. Despite an increase in the trade deficit, higher transfers helped support a narrow deficit in 3Q24. As a result, the rolling-4Q current account deficit remained broadly stable from 2Q24 at 1.8% of GDP (USD 7.3 billion), but below from the 2.0% of GDP in 1Q24 (USD 7.7 billion). At the margin, our own seasonal adjustment shows the annualized deficit sits at 1.5% of GDP in 3Q24, 0.4pp narrower than the 1.9% in 2Q24.

The low CAD deficit in 3Q24 was mainly due to higher transfers and a smaller income deficit. Exports fell 1.8% yoy during 3Q24 (+2.6% yoy in 2Q24), while imports rose 5.2% (+4.1% in 2Q24). Overall, the goods trade deficit widened by USD 1.0 billion from 3Q23 to USD 2.4 billion. Meanwhile, the services balance remained stable at a USD 0.1 billion deficit. Transfers reached USD 4.1 billion (up USD 3.4 billion from 3Q23). The income deficit narrowed to USD 3.3 billion (USD 3.5 billion in 3Q23; USD 4.8 peak in 3Q22).

Foreign direct investment continued to fall in the 3Q, but the overall financing of the CAD remains favorable. Direct investment into Colombia came in at USD 3.3 billion in 3Q24, USD 0.6 billion down over one year. Net direct investment reached USD 2.4 billion (a USD 0.9 drop from 3Q23), resulting in USD 10.1 billion for the rolling year, achieving a 138% coverage of the CAD (180% in 2023; 65% in 2022).

Our Take: The 3Q surprise raises the odds that the CAD will come in at below our 2.5% of GDP call (BANREP’s estimate is 2.2% of GDP). A low CAD could moderate FX volatility to external shocks. Amid a low CAD and falling inflation expectations, we expect the central bank to continue to cut rates. Yet, tight global financial conditions and weak currency dynamics would prevent a majority of the Board from accelerating the rate cut pace. We expect another a 50bp cut at the next monetary policy meeting (December 20) to 9.25%.