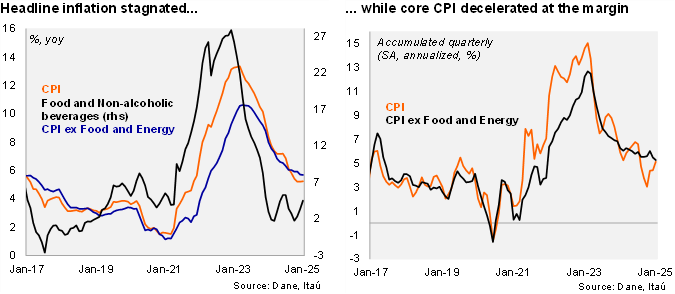

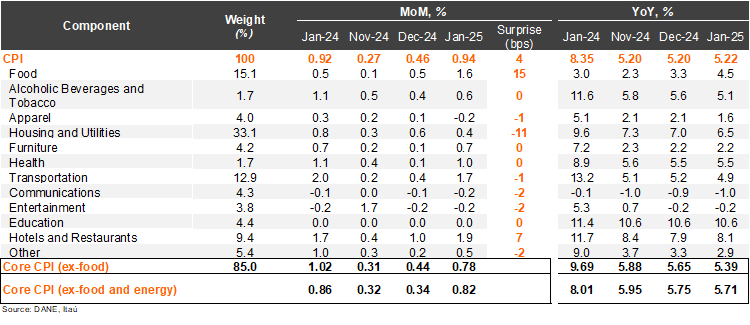

Consumer prices rose by 0.94% mom in January, above the Bloomberg market consensus of 0.81% while closer to our 0.90% call. The main positive contributors in the month were food prices (+1.62% mom; +30bp), transport (+1.71%; +23bp) and hotels and restaurants (+1.90% mom; +21bps). An upside surprise in food prices and hotels and restaurants explained most of the surprise relative to our forecast. Consumer prices excluding food increased 0.78% mom (+1.02% mom one year earlier), while inflation excluding food and energy rose by 0.82% mom (core; 0.86% one year earlier). Overall, annual headline inflation was little changed at 5.22% (5.20% in December). Meanwhile, core inflation dropped by 4bps from December to 5.71% (10.60% peak in April last year; 8.8% at the end of 2023).

Services inflation remains elevated. Non-durable goods inflation (mainly food) came in at 3.7% yoy, increasing 9bps from the previous month. Meanwhile, energy inflation fell to 2.92%, a drop of 210bps from December. Durable goods inflation remained in negative territory at -2.8%, but increased 25bps from December. Services inflation dropped by 4bps to a still high 7.34% (9.51% peak in September). At the margin, we estimate that inflation accumulated in the quarter was 5.1% (SA, annualized; 4.4% in 4Q24). Core inflation fell to 5.3% from 5.5% in 4Q24 (SA annualized).

Our take: The disinflationary process has slowed in recent months. Our preliminary estimate for February’s CPI, to be released on March 7, is close to 1.0% (considering the recent announcement of gas tariffs). However, if the gas adjustment is eventually reversed by a government mandate, a variation between 0.8% and 0.9% is plausible. Moreover, given the higher-than-expected minimum wage increase and indexation pressures, the disinflationary process is set to be slow. We expect a yearend inflation of 4.2%. The slow disinflation process along with heightened global uncertainty could lead the Central Bank board to remain with a cautious stance ahead. However, the makeup of the new Board may tilt the balance towards resuming cuts after the January pause. The next MP will take place on March 31.